Aleksey Chernobelskiy

•November 30, 2023

Do sunk costs matter in capital calls?

On the relationship between capital calls and the sunk cost fallacy

*Welcome to the **72 *subscribers and 14 new premium subscribers who joined since the last issue!

**Last premium post: **5 reasons to invest in real estate syndications

Last free posts: top 15 syndication mistakes and LP Investing Digest #5

🎉 **December promotion: **earn a free month of premium for every friend you refer! Click the button below to learn more.

PS we passed 1,400 subscribers and recently got a “Substack Bestseller” award - thank you very much for all of your support, it means a lot! 🚀

Do sunk costs matter in capital calls?

Here’s the agenda for today:

Introduction to capital calls

Why capital calls aren’t created equal

Introduction to sunk costs / sunk cost fallacy and how they relate to capital calls

Illustration using a model

1 - Introduction to capital calls

Broadly speaking, a capital call is when a real estate transaction runs out of money and needs an infusion of capital.

This should not be confused with a planned capital call, such as the one in a fund structure (e.g. LP invests in a fund and they “call” capital over time as the fund acquires properties, as opposed to calling all of the capital up front before the acquisitions occur) or an ongoing construction project that was intentionally not fully funded at the beginning. For the sake of clarity, the entirety of this article will be discussing unplanned capital calls.

Although unexpected capital calls are indirectly stating that the investment didn't turn out as planned (since the initial capital was supposed to be enough), not all capital calls are created equal.

2 - Why capital calls aren’t created equal

The terms that a GP offers to the LPs when issuing a capital call differ and that won't be the topic of discussion today. With that said, I would like to present two cases to illustrate that capital calls should not carry purely negative connotations because they are not created equal.

Consider a multifamily project that is going according to plan, but the GP ran out of capital as a result of an unexpected cost increase. As an LP, you know that the project is 95% completed and this last amount of capital will get it across the finish line. You also know that if you were to sell the project today your equity is in the money - it is worth the amount that you put into the project, or more.

A different example would be a scenario where an LP invested in a multifamily project and the GP is no longer able to pay the debt service as a result of an expiring rate cap (i.e. the GP paid a certain amount to lock in an interest rate at the time of purchase and this contract that caped the interest rate has now expired). By doing some back of the envelope math based on the income the properties are producing and market cap rates today, you come to the realization that your equity is not worth anything - in other words, you lost the entirety of your investment because the property is worth less than the debt that the property is carrying.

Notice that even though in both scenarios the request from the GP is more money, your decision should be weighed differently. In a later post, I’ll publish a full framework for analyzing the capital calls decision but the topic of today’s discussion will be slightly different.

Sometimes - but certainly not always - the situation can be described as the following:

While the capital call might be a percentage of an LP's original investment and may seem insignificant, it should still be viewed as a new investment. The capital that you are putting into the capital call could be used in another investment, and therefore the return that you make on the additional dollars that you invest should make logical and financial sense.

While the capital call might be a percentage of an LP's original investment and may seem insignificant, it should still be viewed as a new investment.

3 - Introduction to sunk costs / sunk cost fallacy, and how they relate to capital calls

A sunk cost is a cost that has already been incurred and cannot be recovered. The sunk cost fallacy is when people let sunk costs influence their decisions.

Let's think about how the applies to our situation of capital calls.

When you receive a capital call you are already an investor in the property that needs more capital. As such, one might follow the sunk cost fallacy and say “of course I should invest to save the money I already invested,” or “the additional contribution is small relative to my original investment so I have to support this in order to get my capital back.”

Here, I would like to make two separate points:

Using the sunk cost fallacy, or any permutation of reasoning similar to the ones I’ve outlined above, is a poor investment decision with the marginal cash that you are investing. Your marginal investment should be thought of as a new investment decision and not be influenced by your prior investment beyond analyzing the return of making vs not making the capital call.

Having said that, there’s a big complicating factor that’s the topic of our discussion today - in the vast majority of cases not investing in a capital call comes with a form of dilution that penalizes you (as LP) for not investing. This means that, if you don’t invest in the capital call, your original investment will be worth less purely as a result of you not investing additional capital. This interdependency makes capital call decisions complex and creeps into the “sunk cost” discussion.

If you don’t invest in the capital call, your original investment will be worth less purely as a result of you not investing additional capital. This interdependency makes capital call decisions complex and this will be the topic of our post discussion today.

The dilutionary mechanism varies throughout agreements, but we’ll walk through a generalized example below that will work regardless of how the mechanism is structured.

4 - Illustration using a model

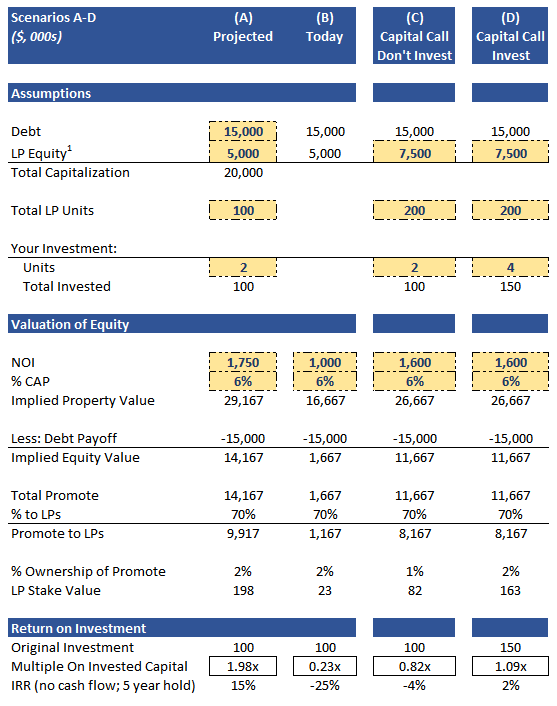

Below you’ll see an illustration with 4 scenarios labeled (A)-(D). I’ll go through all of these in detail below, but first let’s start with scenario (A).

If you’re able, I would recommend opening this in two separate windows so you can look at the model and my commentary next to each other.

(A) - Projected

The Assumptions section illustrates a real estate syndication with a total purchase price of $20 million. The deal had $15 million of debt and the limited partners put up $5 million in equity in order to close the transaction. The $5 million of equity was spread across 100 LP units/shares in the partnership. For the sake of simplicity, I'm going to ignore any transaction costs, GP equity co-invest, and preferred return payments. Notably, I also assume that there’s no return of capital clause, but more on that below in (B).

You personally invested into this syndication by purchasing two units at a price of $50,000 each for a total investment amount of $100,000.

Now let's look at the Valuation of Equity section. At the time of purchase the property was supposed to be sold (after the investment period is over) at an NOI of $1.75 million and the exit value was based on an exit capitalization rate (“cap rate”) of 6%.

This allows us to understand the implied property value at any given point in our scenarios and we subtract $15 million of debt in order to get to implied equity value. Note that for the sake of simplicity, I’m ignoring amortization.

Anything that is left over in equity is split through a waterfall, here assumed to be 70% to LPs. Then you get your pro rata share of ownership using the number of units that you invested in out of the total units outstanding.

Finally, this gets us to Return on Investment. When you invested in this deal you were expecting to earn a 15% IRR over a 5 year old.

(B) Today

Per the GPs reporting, today the property has NOI of $1 million and can be sold at a 6% cap. If the GP decided to move forward with such a sale you can see that you would lose roughly 77% of your investment (invested $100,000 but only got back $23,000).

This is a good time to pause, because it clearly illustrates that properties don't always go up in value - this is an assumption I hear often.

A property’s valuation is dependent on many variables, but it is certainly closely tied to both NOI and cap rates.

Cap rates, by and large, are determined by macroeconomic factors that the GP cannot influence.

NOI, on the other hand, is usually direct consequence of the GPs investment research and operational excellence.

Another great thing to point out here is the return of capital clause. If you’re not familiar with what that means, I suggest pausing to read this article.

You’ll notice that in the model above, the promote split of 70% still kicks in **despite **you losing money as an LP. This is exactly why return on capital clauses are really important - and why I think you shouldn’t budge on them, as I wrote in the linked article above. We have a case here (and Scenario C) where the GP is technically making money via the promote while you (LP) lost money on your original investment.

In other words, this is a case where there is NO return of capital provision - which I do see from time to time in documents. In the event that the return of capital provision is present, Scenarios B and C would be different. That is, in both Scenario B and C, the 70/30 promote would only begin once LPs are fully paid back. For the sake of our example here, I kept the 70% consistent across all cases to not overcomplicate the model (becomes harder to understand and follow).

Now - you open up your inbox and you get a capital call notice from the GP.

The capital call comes with the following terms:

50% of the original equity is needed from all LPs (i.e. $2.5 million in additional funding)

If you don’t invest, you get diluted. There are many technical ways that this can be structured, but I’d like to keep things simple:

Let’s assume 100 additional shares/units were created for a price of $25,000 each (this is a 50% discount to your original investment in 2 shares at $50,000 each). Note that 100*$25,000 is the desired additional capital of $2.5 million. This raises the total unit count to 200, as you’ll see in the “Total LP Units” row.

It’s important to note that the additional equity needed (50% in our case) and the discount/dilution above (50% in our case) are coincidentally the same, but are fundamentally independent variables. Equity needs are driven by a capital need, while the dilution is driven by (typically) pre-negotiated legal agreements.

So, now you have a decision make to make - invest in the capital call, or don’t invest?

If you don’t invest, you simple keep your original 2 of (now) 200 unit, thereby getting diluted

If you decide to meet the capital call, you put up the 50% of original equity ($50,000) by acquiring 2 additional units, bringing your personal investment and unit count to $150,000 and 4 respectively.

(C) Capital Call - Don’t Invest

This scenario represents the case in which you don't invest any marginal dollars into the project.

Note that the cap rate assumption remains unchanged, but I did move up NOI to $1.6 million. This is simply saying NOI will improve from today’s figure of $1 million, but perhaps it might not get up to where the GP originally expected the number to be at the time you invested in the deal.

If you look at the **Return on Investment **section, you’ll see that not investing will lead you to lose 4% (per annum) on your original principal of $100,000 over a 5 year period.

Now, notice that even though losing 4% isn’t great.. it’s a lot better than fire-selling the property in Scenario B. Of course this is dependent on being able to raise NOI back to a decent level, the the cap rates not moving up, as well as the project not needing any more capital beyond this capital call.

(D) Capital Call - Invest

Now, if you decided to take the plunge on the additional $50,000, your IRR over a 5 year hold period would be *positive *2%.

You might ask - why?! How can we can go from -4% to 2% when the fundamental assumptions (NOI and exit cap rate) are the same. The answer is dilution - by not investing, your interest in the “overall” equity pool got diluted.

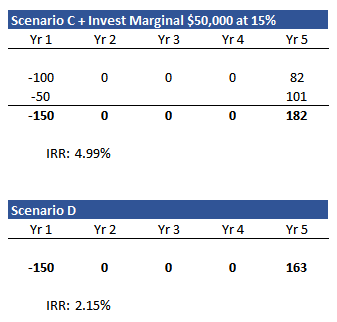

What’s interesting, however, is that the 4% annual loss in Scenario C is based on an investment of $100,000, while 2% annual gain in Scenario D is based on an investment of $150,000.

This is important, because if you invested that marginal $50,000 into another deal that earned you 15% over the same 5 year hold period, you’d end up ahead of Scenario D on the overall investment of $150,000.

I hope this illustrates that, although you should be careful to not fall prey to the sunk cost fallacy when evaluating a capital call request, you should also note that the decision is complex due to dilution.

Thank you for reading! I genuinely hope you found this helpful - the best way to say thank you is to spread the word.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Wealth Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments. I still have 3 spots remaining in the January cohort.

***LP Community - ***free 1,200+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can set up an initial consultation.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.