Aleksey Chernobelskiy

•September 3, 2023

Does a $5,000 LP check make sense?

A guide to sizing LP positions

In an era of low interest rates, everyone became fascinated with passive income

So much so, that in some conversations that I have with LPs I’ll hear comments like:

“How can I possibly lose money on this investment? It’s a multifamily property and everyone needs housing!”

“I need to get out of my 9-5 grind, and the only way out is being an LP so that my money can earn me money”

In my opinion, these views need to change and I’m hoping you’ll agree after reading this.

Today, I’d like to discuss LP check sizing. In particular, what check size is too little.

Crowdfunding has become popular, and it’s common to see LP check sizes at or below $5,000.

The question is, does such a check make sense?

If someone is investing $5,000, it certainly has to be true that they don't have the ability to vet (i.e. conduct due diligence on) the investment. In the rare case that they do, I'd argue that the time they spent on vetting it is a cost that won't exceed their return.

In other words, if someone is spending numerous hours looking at the deck to ensure that this is a good opportunity (which they should do) and ensuring that the legal documents that they’re signing are market (which again, they should do), they’ve already “eaten” through well above $5,000 of cost, which is a 100% return (or 2x multiple on invested equity) on the original $5,000 investment.

Therefore, if you're investing $5,000 as an LP, it must be for one or two reasons:

You don't have much more to invest

You do have a lot more wealth, and you’re essentially gambling to see what happens.

Let’s touch on both:

#1 - “You don't have much more to invest” - **brings us full circle to the quote above - “I need to get out of my 9-5 grind, and the only way out is being an LP so that my money can earn me money.” **I’ll summarize my thoughts in 3 bullets:

In the vast majority of cases, spending the extra hour on your job (as opposed to vetting $5,000 LP investments) will be much more productive use of your time.

This is because a bonus from an employer (1) might exceed anything you’d make from this investment and (2) in many cases also carries a much higher probability of success.

Many people who can only invest $5,000, also can’t lose the $5,000

This brings us back to our other quote from above - “How can I possibly lose money on this investment? It’s a multifamily property and everyone needs housing!”

Investments are risky and if you can’t go into it understanding that you might lose money, you shouldn’t invest

Many people who can only invest $5,000 also need the liquidly (i.e. having the cash around and available) in case something comes up. The vast majority of LP investments tie up your cash for years

So, I think we can all understand that in the case of #1, one should stay away.

**#2 - “You do have a lot more wealth, and you’re essentially gambling to see what happens. **This essentially means that you don’t mind losing the $5,000 and are just hoping this works out. In such a scenario, I have two pieces of pushback:

Why take a chance on something that only has 2xish of upside? In other words, if this is meant to be a risky bet that you didn’t have time to vet, why not invest in something that earn a lot more on the upside?

The downside of real estate and something else like bitcoin are exactly the same - you can lose your entire $5,000. But the upsides are vastly different! So, if this is meant to be a risky play.. might as well try to make 10x to 100x through a venture capital, or cryptocurrency (many more examples) investment

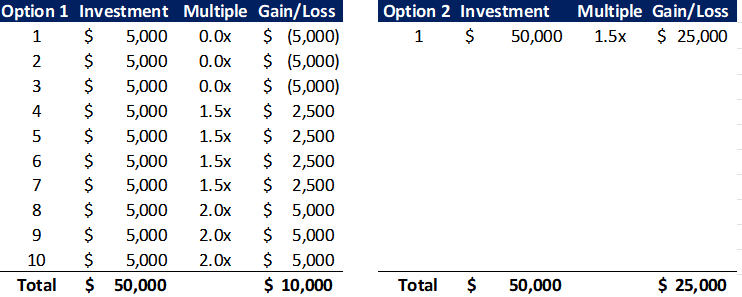

If you don’t have time to vet a $5,000 investment, but have much more capital to invest, why not invest $50,000, but actually take the time to conduct due diligence?

This is a lesson in expected value:

If you make a mediocre real estate investment with the $50,000 that only makes 1.5x (which is considered good, but not incredible, over a 5 year hold), you made $25,000

Compare that with making 10 low diligence investments of $5,000 each. 3 completely fail, 3 return 2x, while 4 investments return 1.5x. Here, you gained $10,000, as illustrated below

If you think “3 completely fail” was aggressive, see here.. still seem aggressive?

So, now that we know that $5,000 is too small, what’s a good number?

**In my mind, a real estate LP investment shouldn’t be less than $25,000. **

Remember that there are fees to get into such an investment, fees during the duration of the investment, and oftentimes fees on the exit (disposition fee). On top of that, there are tax headaches (e.g. waiting for late K1s) and the premium of having your cash liquid should you need it for something.** **

In conclusion, you want an investment to be sizable enough to (1) make sense of spending the personal time on doing diligence and (2) making a real dent on your savings, should things work out. $25,000 will accomplish that for some, but for most I think the number will be above $50,000.

Now that we’ve established a floor on an LP investment amount, we’ll turn to discussing when LP investing is right for you next - stay tuned!

Whenever you’re ready, I could help you in 3 ways. You can click here to set up an initial consultation.

Limited Partners:

Future positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and not sure how to proceed

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide feedback to streamline and professionalize your process

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

**General Consulting **- modeling, strategic advisory, underwriting training, and much more.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.