Aleksey Chernobelskiy

•November 15, 2023

Don't lose money (seriously)

Why capital losses matter more than you think

*Welcome to the **147 *subscribers who joined us since the last issue!

Last premium post: 4 reasons why cap rates are misleading

Last free post: top 15 syndication mistakes

**Announcements: **

**December LP Cohort has 3 spots remaining - **review 4 separate deals together with me and other LPs to learn how to find good LP investments. Simply respond to this email if you’re interested.

Find GPs*** ***in unique asset classes/geographies on my recent monthly intro post (see LinkedIn’s post as well for more)

Don’t lose money (seriously)

In last week’s post, I wrote the following:

One of the most important aspects of investing carefully is not losing your money. Avoiding principal loss is not talked about enough and I will write on this in detail next week. One of Justin Pugh’s favorite quotes is, “money is like soap, the more you play with it the less you have."

I think it’s abundantly clear that understanding the upside of a real estate transaction is important and is ultimately the reason why people invest. Compound interest does wonders. Having said that, I’ve noticed from my LP Advisory work that, when look at an investment opportunity, tend to pay too much attention to upside and not enough attention to downside.

I regularly hear comments like “what do you mean ‘lose money’ - you can just sell the asset.” Many investors will put the probability of losing their money on a real estate investment at 0%, when in reality that’s not the case. You can certainly make a lot of money on an investment, but you can also lose money - I see it daily in my line of work.

Capital loss can take form in two ways:

Temporary - for example, a cash flow payment that was suddenly paused. This creates a loss in income to an LP (important for some, especially if you were living on it), but also pushes off your ability to reinvest that cash.

Permanent - put simply, you invested $500,000 into a deal, and only got back $250,000. This is a permanent loss that you now have to “climb out” of.

Today we’ll talk about the second, since the implications are much more severe to an LP.

First, let’s agree that upside and downside are asymmetrical - they’re simply not created equal.

If you invested $500k and only got $250k back, you need to make a 100% return to get back to where you were even though you only lost 50%.

Needless to say, finding an investment that will earn you 100% (i.e. doubles your money) is not easy, even over a decently long time horizon.

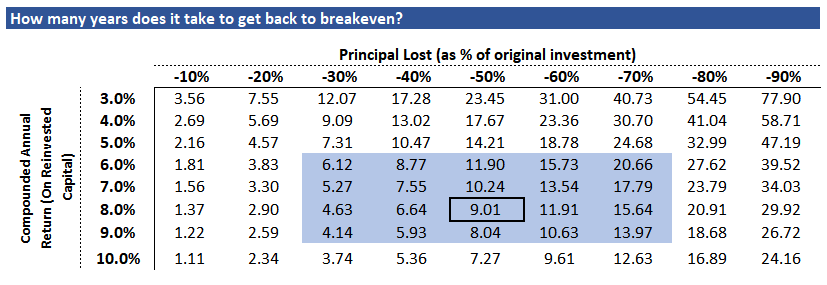

To illustrate this point further, I created (took some thinking - click here if you’re a math nerd) the data table below. Before I give my thoughts, let me just ground you on how it works through an example:

You invest $500k in a syndication (or any investment)

You lose 50% of your investment (find 50% below on the x axis)

You reinvest the remaining $250k at 8% interest (find 8% on the y axis)

It then takes 9.01 years (see the highlighted cell) to get back to your original $500k

What you’ll clearly notice above (see blue highlighted area) is that almost any principal loss in excess of 30% takes many years to recoup. This is why losses matter.

Many people will want to focus on 10% returns (the highest option in the data table for a reason), but you have to keep in mind that replicating those levels of returns year over year (1) is hard and, perhaps more importantly, (2) comes with its own risk of losing capital since those investments aren’t risk free.

While limiting downside is paramount, it’s also important to not stay on the sidelines - all investments come with risk and you need to get comfortable taking it in order to make returns on your money.

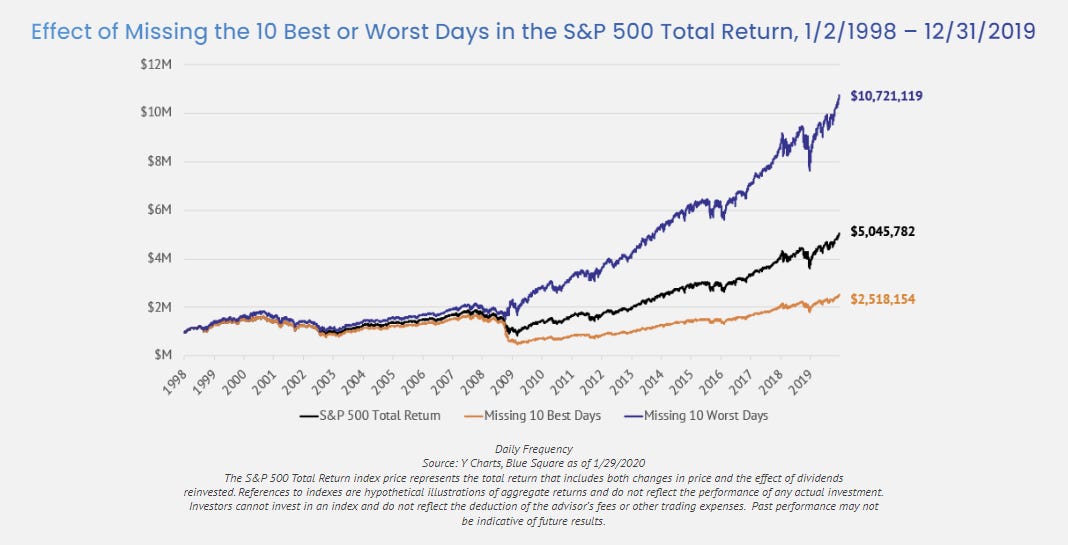

Below is a great representation of the balance an investor needs to take:

- Missing the 10 **WORST **trading days, on the other hand, results in 10x on invested principal (~5 times better than the result above, over the same exact period). This illustrates the impact principal loss has on compounded return, even over a long term hold.

Thank you for reading! I genuinely hope you found this helpful - the best way to say thank you is to spread the word.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Wealth Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments. I have 3 spots remaining in the December cohort

***LP Community - ***free 1,100+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can set up an initial consultation.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.