Aleksey Chernobelskiy

•September 6, 2024

Fees erode more equity than you think

A full example of the impact of fees on investor returns

**Last premium post: **LP Investing Lessons Podcast # 7

Last free post: LP Investing Digest #45 & Full Article Index By Topic

Announcements:

- **LP Cohort: **One more spot in the September cohort. Please reply to this email if it’s of interest, we’ll be starting next week. Review 4 deals with me and other LPs to learn what to look out for in deals.

Fees erode more equity than you think

Happy Thursday! 👋

I spend a lot of time trying to explain why fees are such a big deal, and acquisition fee drag was actually the topic of my first article on August 30th, 2023 (time flies when you’re having fun).

We all know about return of capital (if you don’t, you should) clauses, but in reality getting your capital back after investing isn’t as simple as it sounds.

Today, I’ll illustrate how losing 25% of invested equity day 1 to fees and transaction costs can easily occur in a real estate transaction. This doesn’t mean you shouldn’t invest, but it does mean that you need to be certain that the assumptions are achievable since the investment has to recover that initial loss on equity.

Alright, time to get practical.

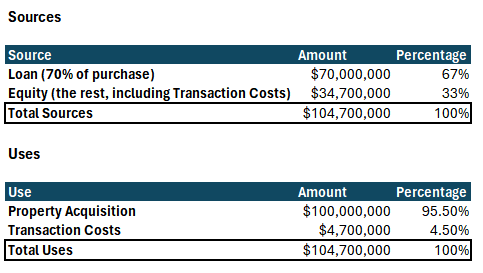

Let’s walk through a $100 million multifamily acquisition with 70% leverage, break down the fees, and show how, in a hypothetical sale at the same price, nearly 40% of the initial equity can disappear.

Deal Assumptions:

Property Price: $100mm

Leverage (Loan-to-Value): 70%

Equity Contribution (30% of purchase price): $30mm

Loan Amount: $70mm

Now let’s talk about expenses to buy such a property:

Note that:

Fees/costs can vary across deals, and in some cases the percentages will be much higher or lower

some of this varies with deal size - larger deals come with lower acquisition fees, for example.

There are also usually considerable fees paid for the lender at acquisition, and sometimes at payoff, which I am currently not including above (this would only make the overall point stronger).

Above, I am assuming there’s a 1% broker’s commission - this varies, and in many cases (but far from all) this fee is paid for by the seller. Having said that, I decided to run with it for the purposes of the illustration .. and the fact that this 1% fee expense could easily be filled up by some other costs/fees

Since these transaction costs are not covered by the loan or original equity of $30mm (which goes to seller), the equity raise needs to increase to account for these costs .. that gets us to a sources and uses table (which you should always look for in a deck, among other things):

On the acquisition, only $30mm actually “made it” (net of fees) to the property investment, even though $34.7mm was invested

On the sale, there’s no cash sitting around to pay the fees, which means we’d have to assume that they come out of closing (i.e. reduce the $30mm in equity after paying off the mortgage by $3.5mm)

To summarize, we just incurred $8.2MM of fees which were a “drag” on the equity investment of $34.7MM, or a 23.6% equity loss… **but you sold the same property, for the same exact price you bought it for! **This is why fee drag is important.

I hope this illustration helped you understand the fees of your next investment. Fees are a very normal part of this business and GPs need them to pay their expenses, but you should also have a full understanding of how such fees impact your net returns.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos in 4 weeks together with me and other LPs to learn how to find good LP investments.

LP Topics Seminar** - **an ongoing biweekly 1 hour meeting with other LPs where we'll go over investment decks, capital calls, distressed situations, and modeling. This is meant to provide a deeper look into existing LP investments. Please reply to this email if you’re interested.

***LP Community - ***free 2,200+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can reach me at aleksey@hey.com.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.