Aleksey Chernobelskiy

•December 14, 2023

Hidden risks of tax benefits in syndications

On tax benefits and the often missed assumptions behind them

*Welcome to the **95 *subscribers and 2 new premium subscribers who joined since the last issue!

Last premium post: An investor's mindset and principles

Last free posts: top 15 syndication mistakes and LP Investing Digest #7

Announcements:

🎁 **New Year’s GP Special: **if you’re a GP and would like to gift 3 months of premium articles to your LPs at no cost to both of you, please reply to this email. If you’re an LP and want to forward this email to your GP, even better!

🎉 **December promotion: **earn a free month of premium for every friend you refer! Click the button below to get started.

Hidden risks of tax benefits in syndications

Many of you have asked about the pros and cons of tax benefits in syndications, and I decided to pair up with Roger after one of his posts because we both feel that this topic doesn’t get addressed enough. Roger posts a lot of great insights for free on Twitter and LinkedIn.

Our agenda for today:

Introduction

Why the promised tax benefits might not apply to you

An example of tax benefits gone wrong

“I’ll just 1031 to not pay the taxes … right?”

Why your GPs CPA matters

1) Introduction

Every LP investor in real estate will tell you the same reasons they prefer private syndications over REITs or the stock market: the tax benefits are amazing! For some other benefits of syndications, see 5 reasons to invest in real estate syndications.

While the tax benefits are truly great, they also carry a few assumptions that might not turn out as planned. Today we’ll discuss four separate risks related to tax benefits so that the below meme doesn’t have to be you! 😊

For starters, here are the three primary tax benefits of investing in a real estate syndication:

Accelerated Depreciation and Pass-through Losses - when a partnership uses investor capital and debt to buy a property, it can take accelerated depreciation on certain assets and that depreciation comes first to LP investors as K1 losses.

This is a good time for brief reminder: an LP has zero control over when a GP decides to perform a cost segregation study (i.e. they might not do it on time or never do it) or when a property is sold. Because both of these have tax implications to you as LP while being outside of your control, they’re important to think about when you’re tax planning.

Tax-free Distributions - when a property has been acquired, improved, and stabilized, typically the GP will refinance the loan and receive proceeds that are then distributed to you as an LP investor

This works from a tax perspective by way of “basis.” Meaning, the IRS will allow investors to receive distributions and not pay tax on them because they have basis either by: (1) their initial capital contribution, and / or (2) debt allocated to them. More on this later!

Further down, we will also discuss later why it’s better to think of these as “deferred” tax-free distributions, a risk many LPs don’t think about

Special Allocations - partnerships have a unique place in the tax code as the most flexible entity structure for determining which partners receive what allocations. Many rules exist as guardrails, but GPs love partnerships because they can receive a promote or carried interest at long-term capital gains rates instead of as a part of a fee - the same long-term capital gains rate enjoyed by LP investors. However, this special allocation can come back to bite LPs if the operating agreement isn’t worded adequately.

2) Why the promised tax benefits might not apply to you

Here we’ll discuss the first of the three benefits above - Accelerated Depreciation and Pass-through Losses.

I often see investment decks that talk more about the tax benefits of a deal than the deal itself (see here for more items in a deck that should give you pause). In the majority of cases, these deals are being marketed to employees with W2 income.

Below Roger and I will explain why this can be deceiving:

As an LP in real estate, the losses allocated to you are “passive,” which means those losses can only offset other passive income. The only exception is if you are a real estate professional AND materially participate in the activity (or make a special election) - in the vast majority of cases, this exception won’t apply to LPs that are reading this.

This is the first risk of a real estate LP - not being able to use allocated depreciation/losses unless you have significant passive income or are a real estate professional.

Let’s make this practical:

Bill is a sales guy at IBM looking to offset his record W2 income with a cost seg study through a syndication

He’s going to be surprised when his CPA tells him that those losses are suspended.

Suspended is the key word - investors don’t lose those losses they can’t take forever, but rather carry forward and offset future passive income (usually capital gain from a sale)

But let’s be clear, Bill did not offset his record year income at IBM, which was his original goal!

There are times when an investor will have enough passive income to utilize these depreciation losses, but this creates a potential tax rate arbitrage risk that’s worth mentioning.

This is the second risk of a real estate LP - using passive losses to reduce passive income that otherwise would have been paid at a low(er) tax bracket.

Said another way, when the property you invested in (and got tax benefits for) is later sold and a significant gain is allocated to the LP, their tax bracket will likely be higher and they will repay recaptured depreciation at a higher rate than when they took the deduction for tax benefits years ago.

3) An example of tax benefits gone wrong

Let's walk through an example where an LP has received tax losses, but then things go wrong when the property is in distress and is handed back to the bank.

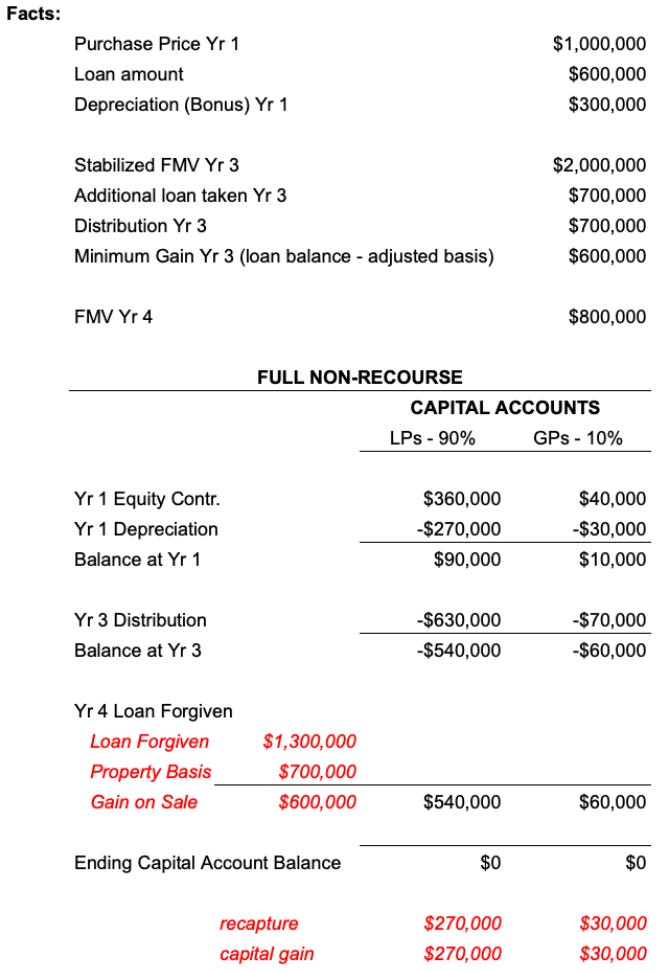

First let's assume that a syndication bought a million dollar property and financed it with $600,000 of debt. We’ll assume here that the mortgage isn’t personally guaranteed (there are some implications if it is, although the larger point still holds) and that the equity was put up by 90% LP(s) and 10% GP. For the sake of example, you can think of yourself as being the entire LP stake, although the impact would be similar for a smaller stake as well.

Some more facts in the model above:

In the first year the sponsor did a cost segregation and passed on $300,000 of depreciation.

By year three the sponsor has improved the property to the point where the fair market value has risen to $2 million (double of purchase price) and there was an additional loan taken out as a result of the increased value in the amount of $700,000.

The $700,000 loan is distributed as refi proceeds

In other words, in year 3 there's a total of $1.3 million of debt on a property that is worth $2 million.

Note that the total cash outflows to the LP (to date) were $360k (at purchase), while the inflows (distributions to LP) were $630k. The LP also got $270k of tax losses that they benefitted from.

Between year three and four, the economy sours and and the property is now worth $800,000 due to expanding cap rates and decreasing NOI. The property goes into distress and the lender forecloses on the loan, getting back the keys.

The result of this exercise is that the LP will be on the hook on a capital gain of $270,000 and a depreciation recapture of $270,000. The tax liability will of course depend on the tax rate that is being paid, but I hope it is clear that the result is both surprising and painful.

If you don’t have the liquid cash to pay this tax bill, you might need to liquidate other investments to pay it.. which is an entirely different challenge that the LP didn’t expect.

This is the third risk of a real estate LP - your tax benefits might come back in the form of a large and unexpected tax bill as a result of distress.

4) “I’ll just 1031 to not pay the taxes … right?”

Said simply, a 1031 exchange allows an investor to delay paying taxes by exchanging from one property to another. This sounds great, and is great (!) - but let’s examine what can go wrong.

The truth is, some people think that if they crush it in a syndication they can “simply” defer the taxes anyway via the 1031 exchange. However, all of these have to be true in order for that to happen:

An exchange can only occur if all the LPs decide to follow along (people might have different preferences)

GP needs to want to do it (GP might need the cash now, and can’t)

The partnership needs to identify something to purchase (which might difficult, you might overpay, or you might simply run out of time)

This is the fourth risk of a real estate LP - if you do really well on a syndication investment, you might be able to 1031 the proceeds. Of course, if the deal did well you’d likely be able to pay your tax liability with your proceeds…but that wasn’t your plan.

For the nerds among us (because this doesn’t apply to most syndications), one of the ways around this requirement is to utilize a Tenancy-in-Common (TIC) structure. In a TIC structure, the existing asset is “dropped down” into separate “tenants” (those that want to sell and those that want to defer). The tenants that want to sell then receive a distribution of their TIC ownership and use that as their relinquished property basis into a new property (under the same §1031 timing restrictions).

But operating TICs and “dropping and swapping” TIC interests to effect a §1031 exchange is not entirely black and white. The IRS has indicated there needs to be positive business intent behind the TIC structure - not just tax avoidance. This takes planning and consideration.

5) Why the GPs CPA matters

The most successful deal (and you personally as an LP) can be impacted directly by a careless CPA hired by the GP. Therefore, every LP should take the time to investigate not only the operating agreement and deal itself, but the standard practices of the supporting CPA who will be responsible for preparing the tax returns for the properties.

Needless to say, you’ll have less of an ability to ask some of these questions if your LP position is relatively small… but I still think it’s important to at least ask a few. At minimum, you should ask:

Who does the accounting for the firm (internal or external) and what’s their background

Do you ever perform third party reviews of the books and/or audits? (this is a lot less common for smaller firms)

Can you give me a few months (or quarters, depending on reporting cycles) samples of your financials included in your reporting packages for a specific property (specifying is helpful, since it’s a more pointed question)

If possible, ask other LPs to see whether the K1s are done on time

Have you picked someone for your cost segregation, and what was the initial feedback (this is especially important if you’re depending on those tax benefits)

We have also included a few more pointers below (from the perspective of a GP interviewing the CPA) that I think will be helpful to all of you, since these decisions have a direct impact on you.

Example questions to determine real estate expertise may include:

How many real estate partnerships do you prepare annually?

What are the main types of asset classes of those real estate returns?

What is your position on cost segregation studies?

What types of tax elections do you typically suggest for your real estate clients?

What types of taxable gain deferral strategies are you familiar with?

Answers from a real estate savvy CPA may look something like this:

How many real estate partnerships do you prepare annually?

You’ll want something more than a handful here. And if it’s a national firm, you’ll want to be sure your manager and partner are on the real estate team.

What are the main types of asset classes of those real estate returns?

Get a breakdown of what rough %s each asset class represents for them and how your investment fits in those categories. You don’t want to be the first type of asset class they have.

What is your position on cost segregation studies?

Generally a CPA should be in favor of these studies, especially on longer hold projects.

What types of tax elections do you typically suggest for your real estate clients?

You’ll want to see familiarity with the below types:

163j RPTOB

§469 Activity Aggregation

Repair & Maintenance de minimis

What types of taxable gain deferral strategies are you familiar with?

Again, something resembling one of the below:

1031s

Tenancy in Common

§754 step-ups (and mandatory step-downs)

Thank you for reading! I genuinely hope you found this helpful - the best way to say thank you is to spread the word.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Wealth Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments. The January cohort is now full, but the February cohort still has 4 spots available.

***LP Community - ***free 1,300+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can set up an initial consultation.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.