Aleksey Chernobelskiy

•December 6, 2023

An investor's mindset and principles

Thought processes and character traits that'll help you succeed as an LP

*Welcome to the **73 *subscribers and 11 new premium subscribers who joined since the last issue!

Last premium post: Do sunk costs matter in capital calls?

Last free posts: top 15 syndication mistakes and LP Investing Digest #6

📰 **We got quoted in The Real Deal: **I continue to advise clients that have capital calls and the The Real Deal reached out to speak. I said “we” because I truly think I wouldn’t be here without all of your support, so thank you!

🎙️**New podcast up** - I touched on a bunch of topics, all related to LP investing. Hopefully the content is better than my beard (see comments to understand the joke)! You can also find the video/audio on Apple, Spotify, and YouTube.

🎉 **December promotion: **earn a free month of premium for every friend you refer! Click the button below to get started.

An investor’s mindset and principles

Some of you may know that prior to advising LPs on real estate investments, I ran a 20 person team at a public Real Estate Investment Trust (“REIT”) called STORE Capital. This experience was fascinating in many ways, but I would like to pull from one particular aspect of it for today's discussion.

There were two aspects to my job:

The first was to manage the existing $10 billion outstanding across ~2,800 properties. There are plenty of lessons to speak about there, but that’s not what we’ll be talking about today.

The second was to oversee the entire team that underwrote any new transaction that the firm was considering. For context, we typically bought well over a billion in properties per year and each asset was usually in the $5-$10 million range - that’s a lot of properties! Now, these figures describe the properties that we actually bought, while the number of properties that the firm passed on due to my team’s underwriting efforts was many multiples of what we bought.

This brings us to today's topic - the investor mindset. Simply said, my job was to vet real estate investments and to figure out whether the risk-reward profile of a transaction met our criteria. A limited partner is put in a very similar situation every time they review an investment for themselves.

I would like to spend some time thinking through the process that helped me be successful at STORE, with the hope that it'll help you apply some similar principles when analyzing your own investments.

It is easy to getting bogged down in the details of a transaction, but many times it’s even more important to “zoom out” after all of your analysis (recommend top 15 syndication mistakes on this point)** **in order to look at the investment as a whole – both the good and the bad parts.

You should think about investments as a muscle – the more transactions you see, the easier it’ll get to compare investments and get to a decision. Although the below (and many of my other articles such as the three pillars of LP investing: Execution, Alignment of interests, Property) are meant to shorten the timeline of your practice, there’s simply no shortcut to educating yourself and doing the reps.

Alright, let’s dive in:

1) Healthy dose of skepticism

It is always a good idea to assume that someone passed on a deal before it got to your inbox, regardless of your relationship with the counterparty. 9/10 times this is actually true, and even if it isn’t true it’s generally a good principle to stand by when investing.

A few related corollaries that are generally true, in a probabilistic sense:

The "exclusive" opportunity to invest was blasted to hundreds of people and rejected by at least one person before you saw it

When someone tells you that you were their first call, it's usually not true (sorry, but this statement is true across a large enough sample size)

Most "off-market" deals aren't truly off-market

Having said that, the skepticism needs to balanced with action - stashing all of your cash under the pillow or putting it into treasuries is also not the right long term answer. Bias towards action while staying pragmatically optimistic are both good ways of thinking about counterbalancing this skepticism in order to truly make it a “healthy” dose.

Skepticism needs to balanced with action - stashing all of your cash under the pillow or putting it into treasuries is also not the right long term answer.

Said another way, you can always find reasons to say no to a deal, but the key is to find enough reasons to say yes while considering the entire risk profile. One way to do this, is to focus on the main variables in a transaction that are often referred to as catalysts.

2) Search for the top 3 positive and top 3 negative catalysts

As you’re going through a deck, keep asking yourself:

What assumption is being made

What can go really right or wrong with this assumption

How does such a change in the assumption impact the overall transaction (and ultimately your return)

If you do this enough times, you’ll be able to swift through investment offerings much more efficiently. No deal is perfect and they all carry certain risks - but in many circumstances the positive catalysts or negative catalysts might make the decision for you.

As you take note of such catalysts, make sure you’re aware what assumptions are being made in the offering and look for sensitivity tables to get you comfortable with the downside (and upside, although decks generally do a better job explaining that part 😊). Be conscious of how macroeconomic events (that are outside of the GPs control) can impact the property, especially negatively.

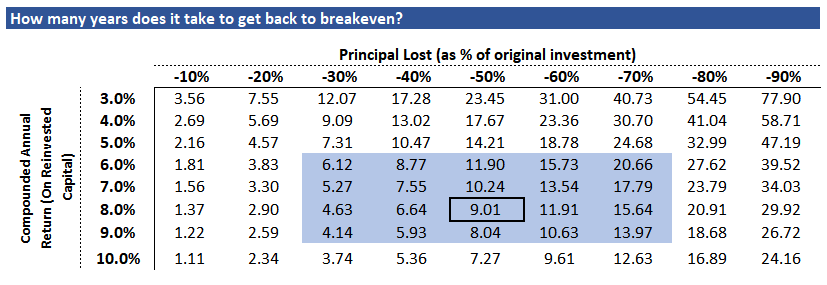

One parting note on this topic - uncertainty will exist in every investment, but there’s a big difference between investing in something knowing the uncertain vs investing blindly. There are known unknowns - you should find them in any deal and expect a sensitization from the GP to understand how returns are impacted if things don’t go according to plan. Be mindful of the heavy impact of losing your principal as well as the upside potential of the investment (if the upside is limited, the downside should be as well). Two downside catalysts can also occur at the same time, which is why two variable data tables are helpful, such as the data table below from the article on not losing your money.

Uncertainty will exist in every investment, but there’s a big difference between investing in something knowing the uncertain vs investing blindly.

3) Counterparty incentives

This is the principal–agent problem, which you should be deeply familiar with as an investor. I cannot tell you how many times this factor alone saved me from making poor investment decisions.

Imagine you hire someone to do a job for you, like a handyman to fix your sink. You're the "principal" (the one who hires and has the principal to pay the cash), and the handyman is the "agent" (the one hired to do the job). Now, the problem is that the handyman might not always have the same priorities as you. They might do a quick fix to get paid faster, even if it means the problem will come back later. So, the principal-agent problem is the challenge of making sure the agent acts in the best interest of the principal, despite their different motivations. It's like trying to ensure your sink gets fixed properly, not just quickly.

Now, back to investments - you should always be thinking about who’s in front of you, who else is in the deal (e.g. lenders, developers, and any other parties) and how they’re all incentivized in a direction that aligns with your goals.

As an example, if you're investing in someone who's investing in a deal for you, you are likely getting charged twice and will make significantly less than the LPs that are direct to GP. There’s nothing wrong with this, as long as you understand the implications and are truly given the value you’re paying for by the intermediary. Train yourself to ask “why” and “how are you getting compensated” - it’ll serve you wonders.

It’s critical to understand the incentives of your counterparty – what needs to happen for them to win big, and do they still make money off of you (today or later) if the deal turns sour. Generally speaking, the latter is critical and is often missed. If the deal turns sour at some point in the future, will the GP still be incentivized to carry it through to maximize the value of your investment? You can find a lot more on the topic of alignment of interests in the second pillar of LP investing - there’s a reason why this is the second pillar and is in front of evaluating the property (the third pillar).

4) Understanding the investment landscape; a money mind

When looking at any investment you have to understand that this is only one transaction that you could invest in within a given asset class, but perhaps more importantly one out of hundreds (tens of thousands?) of other opportunities that you could invest in more broadly. This touches on portfolio allocation and understanding how to compare risk and reward across different investment opportunities, which will be the topic of a later post. For today, I would like to touch on the fact that there are ample investment opportunities regardless of how unique you might think the opportunity in front of you is.

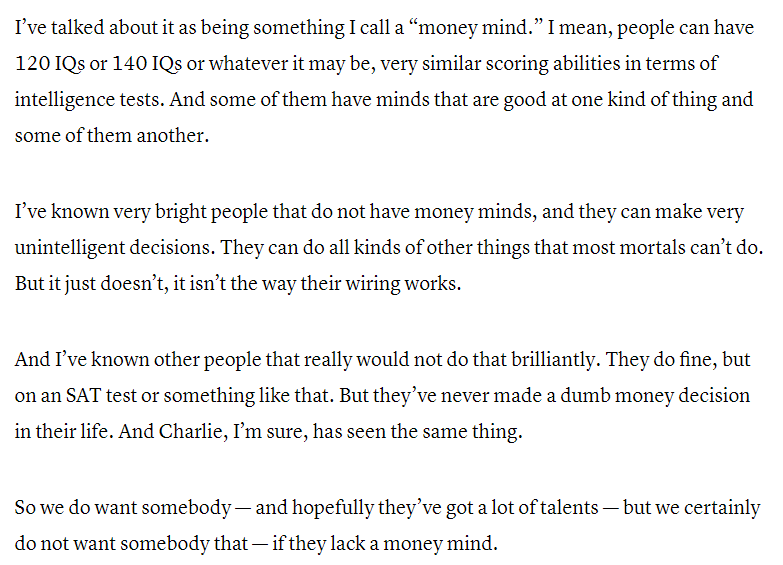

In a 2017 annual shareholder meeting, Warren Buffett was asked how he would look for the next leader of the company. You can watch the full answer here (see topic #33 in the link and the video will sync to the right place immediately), which is fascinating in its own right, but I would like to just point out one relevant excerpt below.

As you see above, Warren Buffett distinguishes between intellect and having a money mind. I think the same holds true when it comes to wealth. Wealth creation vs preservation require different skillsets. Moreover, the same traits that got one to incredible wealth, can also be the traits that forces them to lose it all. Accredited investor status is tied to wealth as opposed to investment acumen, and I personally think that it can give people a false sense of security.

In the context of our conversation, having a money mind simply means that there are many ways to make wise money decisions and this particular deal in front of you isn't the only path. A money mind is acutely aware of downside risk and its impact on the overall investment decision regardless of asset class. A money mind also learns consistently, particularly from their own mistakes, as opposed to putting the blame on others.

A money mind also learns consistently, particularly from their own mistakes, as opposed to putting the blame on others.

5) A willingness to ask questions and walk away

I can't tell you how many times I speak to LP investors that are nervous to ask questions or walk away from a transaction. Sometimes people invest based on the fear of missing out (an entirely different topic that I’m sure you can already predict my opinion on), but this is something entirely different - people investing because they don’t want to ask questions and/or don’t want to upset the GP by not investing.

Some of this hesitation comes from asking what might be perceived as a stupid question, but a decent majority comes from people who don't want to lose the pipeline of new deals from that sponsor as a result of “annoying” them with questions. For a minute, I would like to address both of these.

In the case of the first - being afraid to ask a stupid question - this doesn't seem like a real concern. Either the question (1) has been thought about hundreds of times and the answer is very simple to the sponsor or (2) the question is difficult and requires thought. The first is what I would call a layup for the sponsor, and one might even argue that answering such a question gives the sponsor an ability to stand out (by giving a thorough response and explaining it well to you). The second just means that you have asked a great question! Either they think about the difficult question and answer it well, or you avoided a problem - both great outcomes.

In the case of the second - being fearful of losing the pipeline of new deals by asking a question - doesn’t make logical sense either. Remember that a GP can't acquire a deal without your money. Of course, they might find that money elsewhere … but it is also true that you can find many other investment opportunities as we've discussed above in #4. Perhaps the best way to summarize my opinion on this fear is don’t fall in love (or invest, in our case) with something that will never love you back.

Thank you for reading! I genuinely hope you found this helpful - the best way to say thank you is to spread the word.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Wealth Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments. I still have 2 spots remaining in the January cohort.

***LP Community - ***free 1,300+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can set up an initial consultation.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.