Aleksey Chernobelskiy

•March 7, 2024

Single tenant net lease syndications

Why that 1031 "mailbox money" investment is more complex than you thought

*Welcome to the **53 *subscribers who joined since the last issue!

Last premium post: Why most LP investments won't 2x your money

Last free post: LP Investing Digest #19

**

If you just joined:** I write twice per week and you’ll receive those emails as I post them. One article is always premium (such as this one), while the other is a free weekly digest on LP topics that might be helpful to you. If you’d like to upgrade to premium (which includes access to full archive of my articles), you can do so here:

Single tenant net lease syndications

Welcome back 👋

Someone sent me a message today asking about single tenant net lease investments. Although I was in the middle of writing another article (it’s on the “quitting your 9-5 marketing strategy” - stay tuned!), I got excited and decided to write this one instead.

If you’d like to submit a topic leave a comment below.

Today we’re going to dive deep into Single Tenant Net Lease (“STNL”) assets, which is what I focused on while I was at STORE Capital, one of the largest players in this space. This is a very common asset class among syndications (especially via 1031 exchanges and DSTs, which I touched on here).

I hope this exercise will help you understand why STNL investments aren’t as simple as many brokers or GPs make them out to seem.

Today's agenda:

What is a single tenant net lease (STNL) investment?

Isn’t buying a single tenant building more risky for the investor?

What is a sale-leaseback and why do they exist?

When do sale-leasebacks occur?

Let’s dive in.

1) What is a single tenant net lease (STNL) investment?

STNL investments are free standing buildings that are leased to one tenant.

A few examples:

childcare

car wash

restaurant

movie theatre

furniture store and other retail stores

light (e.g. food processing) and heavy (e.g. metal fabrication) industrial buildings

The above are just a few examples, while the truth is that any freestanding building with a business inside would be considered a STNL deal as long as the lease is triple net (“NNN” - i.e. tenant is responsible for all expenses at the property including property taxes, insurance, etc.)

STNL tends to be categorized under retail, and this couldn't be further from the truth. Are some STNL investments retail? Yes. Are most? Absolutely not.

Many buyers in STNL choose to only transact on profit center real estate, which can be loosely defined as a building that has a P&L (income statement) attributed to it. A counterexample to this could be an office building, where it’s harder to measure/track importance of the building to the tenant’s core operations.

2) Isn’t buying a single tenant building more risky for the investor?

All else equal, having more tenants does diversify risk. Said simply, if a tenant defaults, you lost your entire rent stream… and are now forced to replace it. In some cases, you’ll be able to find a tenant who pays the same amount (or more) in rent, but in other cases the replacement rent will be substantially lower than what you were receiving before … and situations like these can cause distress.

Now, the problem with the first sentence above is that it began with “all else equal”.

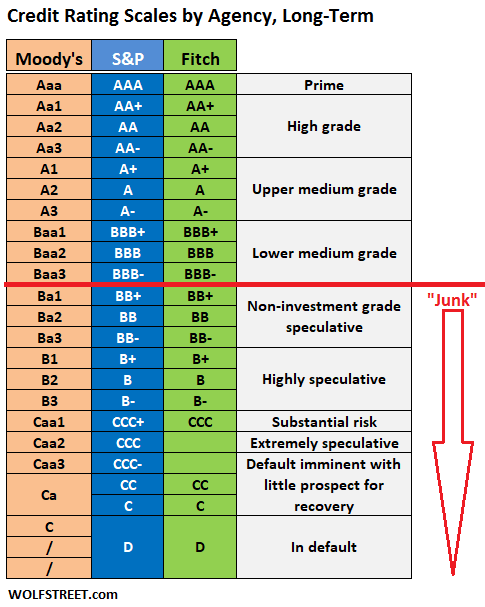

Because the NOI is typically fixed in STNL transactions (other than rent bumps), and you only have one rent stream, it’s critical to understand who your tenant is. In the non-investment grade (“non-IG”) universe (see image below for credit ratings by the different agencies) it’s common to do deep dives into the business to understand how the business is doing in an attempt to understand its creditworthiness. This is especially important when you’re getting into a long term lease with your counterparty, whereas shorter term leases with high demand tend to focus a little less on credit quality.

Now, let’s address the other side of this.. many investors only buy IG (investment grade) assets (often with very little financial reporting) because it’s “mailbox money.” The truth about this is that it’s true… until it’s not.

When I say this, I don’t even mean that the tenant defaults (that’s certainly a lot more common in non-IG contracts than IG ones across a large enough sample size), but rather that the company’s business becomes slightly less safe and the credit gets downgraded. Below is an example of that with one of the most famous 1031 tenants - Walgreens.

The value of a single tenant property is at least partially dependent on the creditworthiness of its tenant, and as such, being a landlord on a property that had a downgrade means that your cap rate (and therefore valuation) just changed - and you can’t do a thing about it!

So, remember.. credit is transient.. some of the largest and safest companies eventually went extinct.

In STNL assets, NOI is generally hard to move (usually only through rent bumps), unless you’re specifically targeting properties with lease expirations coming up so that you can release them. Because of that, these assets (regardless of whether they’re IG or not!) are very sensitive to cap rates.

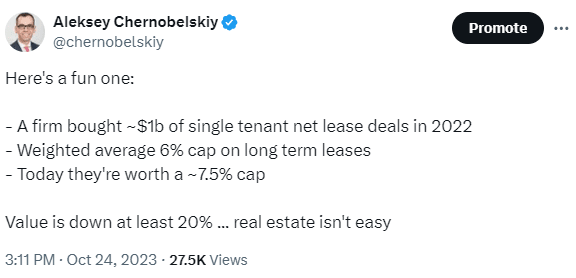

Here’s an example of that - you can apply a 6% cap to $100 of assets to get to your NOI ($6), and then divide by 7.5% to figure out what those assets are worth today ($80).

Now, hopefully the assets are still paying and you’re making debt service with no issues. But nevertheless, I think this is a good reminder of how sensitive some assets are to macro movements.

Lastly, I’ll mention two more important points:

The strength of a single tenant lease is tied to whichever entity guarantees your lease. If your lease is with a single LLC that is only tied to a single property (vs having a lease or guarantee with the holding company that holds the company’s entire operations), you carry a lot more risk as a landlord, since your lease can be rejected through a bankruptcy proceeding.

If there’s a bankruptcy proceeding (e.g. your tenant files for bankruptcy in the middle of a contractual lease agreement) there’s typically a binary (accept or reject) decision on all leases that are tied to such company. Having a master lease (where more than one location are in a single lease) gives the building owner more leverage in these negotiations. Example of this below:

So, in summary:

When compared to most other CRE asset types, a sophisticated owner of a STNL asset knows a lot more about:

chances of lease default and

result of a default (how the default is likely to play out in terms of your investor returns).

3. What is a sale-leaseback and why do they exist?

A sale-leaseback (“SLB”) exists to allow the owner of a business to unlock their equity from the buildings that they operate in. In many cases, a STNL real estate investment started with a sale leaseback transaction at some point in the past, so it’s relevant for us to understand how this market works.

Example:

Child care operator runs a 15 location operation

Currently has 60% LTV mortgages on the properties

The real estate that they occupy is worth $100MM

A SLB across 15 locations would allow the owner to "unlock" the equity (in our example $40MM), while remaining in their buildings long term

The proceeds from such a transaction typically lead to higher return on equity on the business ventures (e.g. buying another business, capex)

If you're driving down a street and see a free standing building with one tenant inside … chances are the owner of the business is the owner of the real estate. Also, there’s a good chance that they haven't thought about the benefits of a SLB.

4. When do sale-leasebacks occur?

There are typically 2 events that trigger a SLB:

Change of control - firm is buying a business and selling the real estate in conjunction with the purchase (to fund a piece of the overall transaction cost)

Family Planning - the family wants to cash out, with proceeds being used for other ventures, the existing business, or estate planning

A STNL SLB provider (i.e. the future owner of the real estate that would lease the asset to the previous owner) would come to closing table with cash for both of these.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments.

***LP Community - ***free 1,800+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can set up an initial consultation.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.