Aleksey Chernobelskiy

•March 1, 2024

Why most LP investments won't 2x your money

A model approach to understanding the search for risk adjusted returns

*Welcome to the **104 *subscribers who joined since the last issue!

Last premium post: 6 steps to a successful capital call decision

Last free post: LP Investing Digest #18

**

If you just joined:** I write twice per week and you’ll receive those emails as I post them. One article is always premium (such as this one), while the other is a free weekly digest on LP topics that might be helpful to you. If you’d like to upgrade to premium (which includes access to full archive of my articles), you can do so here:

Why most LP investments won't 2x your money

Welcome back and sorry in advance for the late night post (I think it’ll be worth it)! 👋

Today I’d like to explore a modeling approach to why investing as an LP isn’t easy.

It should feel hard to find a deal that will double your money over a 5 year period (15% IRR).

Your job as an LP is to have a healthy dose of skepticism - you will pass on many more deals than you invest in. Eventually the hit rate will improve as you get familiar with a sponsor (but don't over allocate!!) and underwriting.

What we’ll do today is make a simple set of assumptions and I’ll show you a model you should recreate from scratch yourself. Then we’ll see what happens from a returns perspective when we start playing around with the variables.

I hope this exercise will help you understand why finding 2x deals for GPs is hard…and why it’ll be hard for you to. Having realistic expectations is really important.

Let’s dive in.

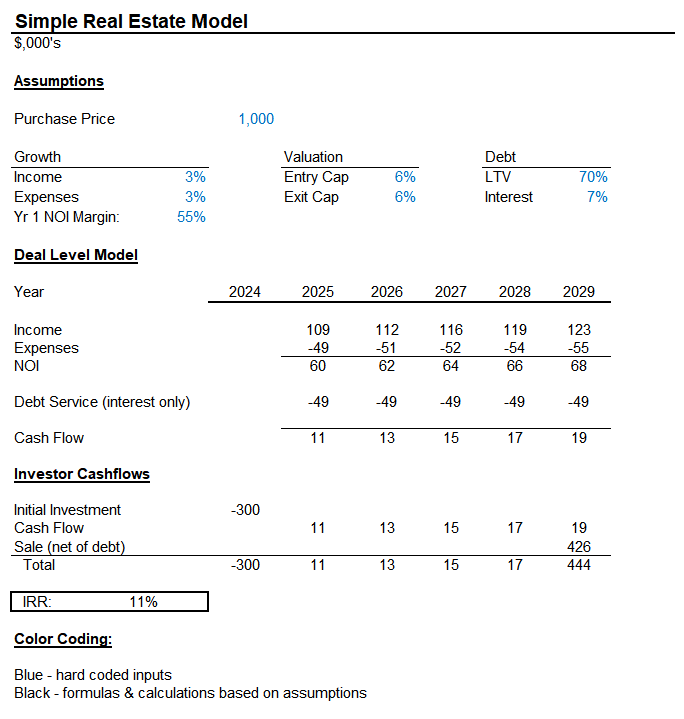

Below you’ll see a simple model (it’s in the name!) and I made it simple for a reason - so you can recreate it yourself. I highly recommend doing this so you can play around with the numbers and learn.

The assumptions are up top, and there’s nothing extraordinary there - these are meant to be assumptions that you’ll see in deals all the time today.

Note that all of the numbers in black are calculated based on formulas, so essentially everything in the model is determined by the assumptions (in blue above).

A few quick points:

Back into $60 NOI (numbers are in thousands) using the entry cap rate of 6%

$1,000 Purchase Price is financed with 70% interest only debt… amortization would be easy to add, but I think it only complicates our topic for today so I didn’t put it in for the sake of the exercise

Yr 1 Income is determined by the NOI Margin of 55%… $109 in income with a 55% margin would get us to the $60 NOI above in #1

From a time value of money perspective, assume that each year represents Dec 31st of ____… so you closed on this December of 2024

Now notice that given these set of fairly basic assumptions, we landed at an IRR of 11% (not enough to double your money over 5 years, which requires 15%!). But then it actually only gets worse:

If you’re an LP, part of this 11% gets split with the GP after a given preferred return… so the return to you will be lower

There are no fees in this model! As I discussed in a previous article, the acquisition fee alone can cost you 10-25% of your equity before you even close on the investment. Then there are broker fees, financing fees, guarantor fees, closing costs, property management fees, asset management fees, …. I think you get the point. Then you get to selling the deal, and there might be a disposition fee … along with all the regular closing costs related to selling a transaction.

So with that, I think we can all agree that although we’re not looking at such a terrible set of assumptions, after fees, you’re not going to make bank.. as they say. The 11% will be dragged down to significantly less, and might make you wonder why you invested in the first place. There might have been tax benefits, sure, but they also don’t apply to most people.

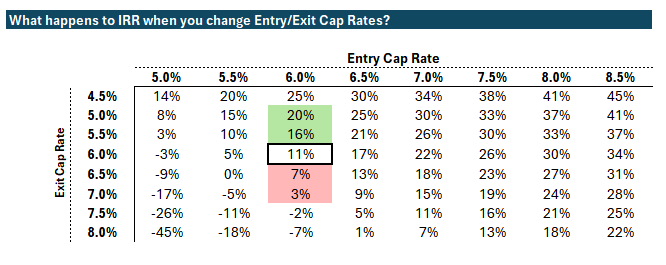

Ok so now let’s have some fun.. what happens if we change some assumptions?! As we go through these scenarios, keep in mind that all of these IRRs are BEFORE fees, costs, and splits (i.e. those will only make this worse for the LP IRR)

Scenario 1:

In green, as expected, you see that if you end up selling at a lower cap rate than you entered at you pick up additional return.

This is called cap rate compression and is part of my top 15 syndication mistakes article because, unlike operations, cap rates aren’t in the control of the GP

As I mentioned in the aforementioned article, changing one (!) variable - the exit cap rate - can have drastic impacts on your IRR. And remember, models are such assumptions and it’s your job to vet assumptions prior to investing.

In red, you’ll see the impact of selling the deal at a higher cap rate than you bought it for… you’ll notice that there isn’t a ton of room for error here, which is why it’s so important to understand these assumptions up front. There’s nothing wrong with investing in a deal that has cap rate compression, as long as you understand that this is the case and are fine with that risk.

There’s nothing wrong with investing in a deal that has cap rate compression, as long as you understand that this is the case and are fine with that risk.

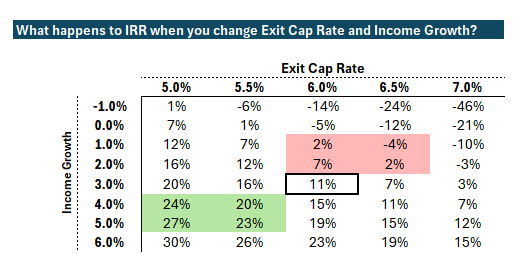

Scenario 2:

Now we’ll change two other variables.

In red, you’ll see that income growth being too high can have big implications to your IRR (we only changed one variable if you go up from the 11% number… then you can go right where exit cap rate is increased)

In green, you’ll see how strong of an impact two variables (rent growth going up and exit cap rates compressing) can have on your returns … this perfect set of events happened a lot of during the past few years.

Scenario 3:

Finally, what happens if nothing happens to cap rates - you bought at a 6% .. and you’ll sell at a 6%. You’ll be fine, right? Not so fast…

In red, you’ll see the impact of both variables moving against you (and recall we’re ignoring all fees, costs, and splits)

In green, you’ll see the tailwinds that these variables can provide you

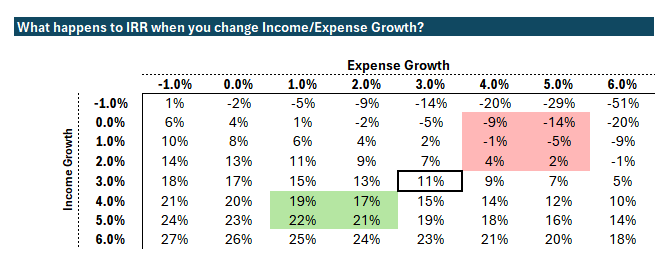

So, what did we learn?

Every GP works very hard to try to find deals that match their criteria.. and hopefully now you understand how difficult it is to get to what I would call a conservative 15% LP IRR.

If you, as LP, get a 15% LP IRR deal in your inbox you shouldn’t assume that it’s right and have that healthy dose of skepticism. Because most “average” deals don’t get there… as we saw above!

Note that NOI and Cap Rate are two very important variables in terms of returns and valuations. We saw what happens when Cap Rates compress or expand - big impacts to returns.

The variable we touched on less is NOI - although we assumed rent growth and that helped NOI substantially over a 5 year period, the deal wasn't so speculative in nature.

As the deal type gets more speculative (e.g. value add) two things happen - your chances of a 2x go up because you’re trying to increase NOI substantially (i.e. by more than just rent increases we assumed above because rents aren’t at market or renovated units will command higher rents) but, and this is important, so does your risk. There’s nothing wrong with investing in something risky, as long as you’re aware that it’s risky and try to figure out what those risks are before you invest.

While keeping all of the above in mind, you have to remember that you can’t get analysis paralysis.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments.

***LP Community - ***free 1,800+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can set up an initial consultation.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.