Aleksey Chernobelskiy

•June 18, 2024

What to know about K1s before investing

Important Schedule K-1 details for LPs

**Last premium post: **Minimum Viable Reporting Package (related to Minimum Viable Deck)

Last free post: LP Investing Digest #34 & Full Article Digest

If you just joined: I write twice per week and you’ll receive those emails as I post them. One article is always premium (such as this one), while the other is a free digest of LP topics that might be helpful to you. If you’d like to upgrade to premium (which includes access to the full archive of 70+ articles), you can do so below.

You can always reach me at aleksey@hey.com & follow my free posts on LinkedIn & Twitter/X.

What to know about K1s before investing

Welcome back! 👋

I get a lot of questions about K1s and find that many LPs don’t understand them to a degree I would suggest before considering becoming an LP.

I’m excited to bring back Roger on our third collaboration. The first two tax related articles are below. Roger posts a lot of great insights for free on Twitter and LinkedIn.

Our agenda for today:

The Basics

Applications to Real Estate

Challenges with K1s

Reading a K1

Let’s dive in:

The Basics

The best way to describe a K1 is that it’s a W2 for investors.

K1s are used by pass-through entities (Partnerships and S-Corps) to report the allocated income, loss, gains, and distributions of the entity.

Just like a W2 reports to you (and the IRS) how much in wages you were paid and how much was withheld already for taxes, K1s report to you (and the IRS) all the income or loss that the IRS will expect to see on the investors tax return.

A Partnership (or S-Corp) will produce a separate K1 for each partner (or shareholder) who will then report that K1 on their tax return.

Practically, this means that the GP has to produce a K1 for each partner and that an LP (individual) has to receive a K1 for each one of their investments.

Application to Real Estate

Partnerships are the favorite federal tax entity for holding real estate for several reasons - flexibility in allocations, favorable debt basis treatment, and friendly distribution rules to name a few - so it’s natural that investors in real estate syndications should expect to receive K1s.

And because of the ability to “pass-through” losses from depreciation (“paper losses”) to individual tax returns, potentially offsetting other income (“cash income”), these investments have continued to use a Partnership structure.

Challenges with K1s

All investments come with some hassles, but I think it’s important to know the challenges with K1s before getting into syndications. Here are a few to consider:

Timing - New investors will often be surprised at the need to file an extension while waiting on K1s. For any number of reasons, K1 production can drag well outside of the April 15 due date and into the summer. The extensions could cost some money as well.

For this reason, and if you’re sensitive to this, it’s a good idea to ask a GP when they issued their K1s in the most recent year and whether they had any delays

There are several practical solutions that are available for those waiting on a refund, however, but the most common one is to file early without the K1 and get your refund. Then when the K1 is ready, file an amended return with likely no change if there isn’t substantial passive income to offset. This doesn’t necessarily raise an audit flag because no additional refund is requested.

Tax Benefit Surprises - more on this in hidden risks of tax benefits in syndications, but simply said many new LPs get upset when they their long-awaited K1s don’t change their tax refund at all. That is because syndication losses for normal W2 investors is passive by default and only would help to offset other passive income.

Costs - many K1s as a result of several LP investments will likely increase the complexity (and therefore also cost) of hiring a CPA

Amendments - amended K1s can cause some challenges/surprises to an LP as well as cause unexpected tax consequences. Of course, this isn’t the norm and only applies when something changed on the underlying partnership tax return associated with the original K1.

State Tax Filings - syndicated real estate deals often operate in multiple states. K1s may indicate income sourced from various states, requiring LPs to file tax returns in multiple states, each with its own set of rules and deadlines.

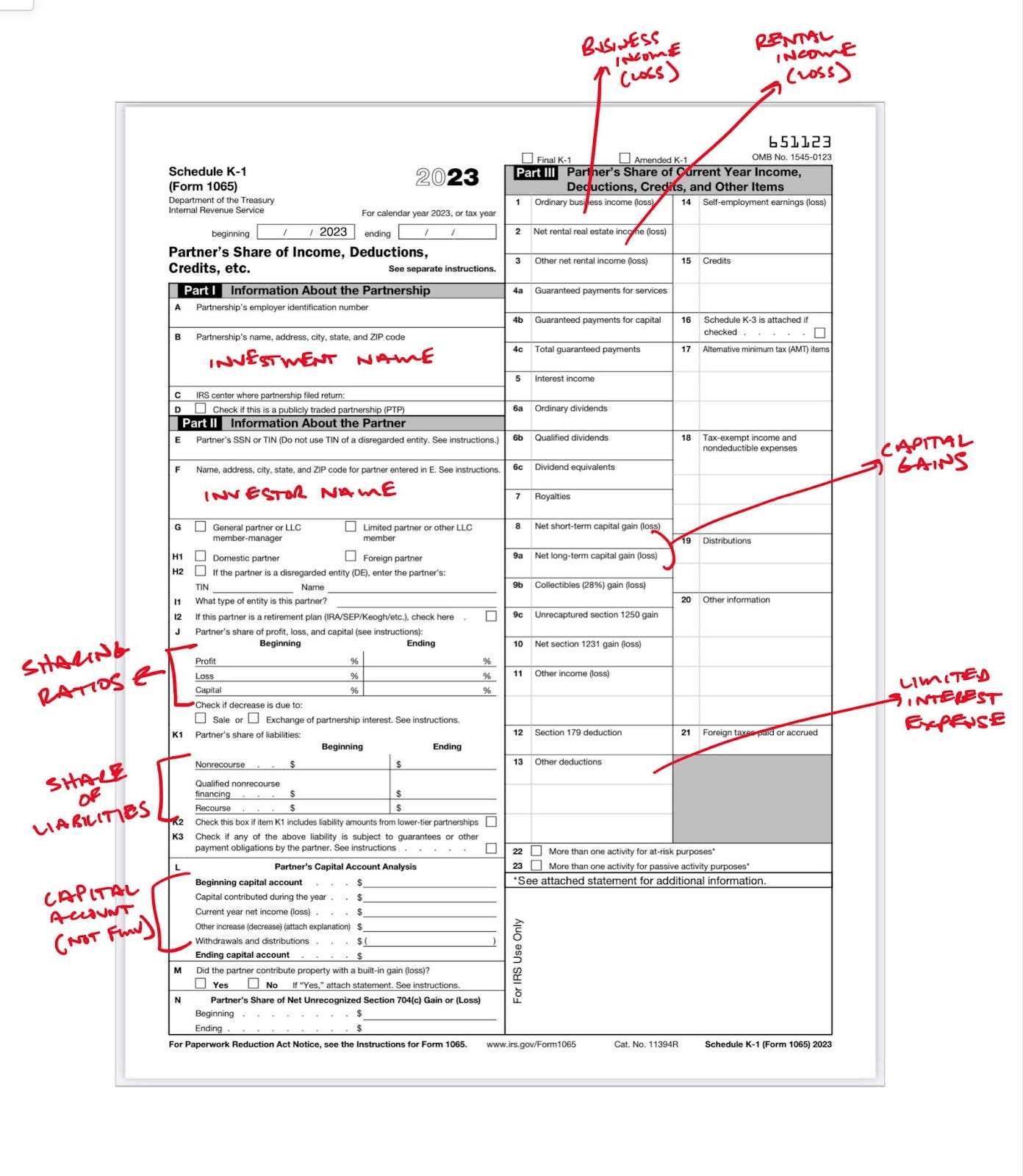

Reading a K1

Below is a screenshot with call-outs of the primary information used and allocated on a K1. We’ll start with the left hand side - this is primarily informational and of course you should consult a CPA for your own case.

The Sharing Ratios are dependent on several factors, including the operating agreement, the original contributions, carried interest terms, etc. Many practitioners will simply put “VARIOUS” due to the fluctuation in these from year to year based on the various inputs.

The Share of Liabilities section represents how much in partnership debt this individual partner is being allocated.

Nonrecourse is what it sounds like - no individual partner is “on the hook” for that liability (think accounts payable).

Qualified Nonrecourse is specific to real estate and is debt from a financial institution secured by income producing property. This type of debt is eligible for special treatment for purposes of taking losses (at-risk).

Recourse is then also what it sounds like - this partner has personal liability for the partnership debt in this amount.

Liabilities are important to allocate properly because Qualified Nonrecourse and Recourse debt increase debt basis which can be utilized to take losses against.

Of note, the Capital Account reconciliation **does not **equal the current valuation of your interest in the property. Rather, it’s a tracker of your investment more akin to a cost-basis method. It records your cash contribution minus all distributions minus losses (or plus gains) allocated to you. The activity shown represents the current year only of activity (income / losses and distributions).

The Capital Account reconciliation **does not **equal the current valuation of your interest in the property.

The right hand side of the K1 is the more quantitative part. It includes the allocated items of income, gains, and losses. Many of these boxes can be subdivided into dozens of sub-codes that you need to skim the K1 footnotes for. But in a income producing real estate investment, you’ll likely just be looking at Box 2 for your share of income or loss.

I hope this was helpful! What would you add?

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments.

***LP Community - ***free 2,200+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can reach me at aleksey@hey.com.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.