Aleksey Chernobelskiy

•October 10, 2024

Cap rate compression trap

How to find hidden cap rate compression in real estate investments

**Last premium post: **LP Investing Lessons Podcast #9 (now on Spotify)

Last free post: LP Investing Digest #50 & Full Article Index By Topic

Announcements:

**LP Cohort: **Review 4 deals with me and other LPs to learn what to look out for - please reply to this email if it’s of interest.

LP Topics: a more advanced ongoing biweekly 1 hour meeting with other LPs where we'll go over investment decks, capital call / distressed situations, and modeling. Please reply to this email if you’re interested.

Cap rate compression trap

Happy Wednesday! 👋

I know what you’re thinking - “how hard can it be to check for cap rate compression!”

If the going in cap rate is 6% and the exit cap rate is 6%, I should be fine.. right?

Today we’ll deep dive on cap rate compression assumptions and why this statement is wrong.

Let’s first understand what cap rate compression is:

Cap rate = Net Operating Income (NOI) / Price.

As cap rates fall, the value of the property rises, making it seem like a good investment even if nothing about the property itself has improved.

If you want to familiarize yourself with cap rates a big more, I’d recommend reading 4 reasons why cap rates are misleading.

Cap rate compression refers to a decrease in a cap rate over the hold period of an investment

In English, this means that the GP expects the property (via supply/demand factors) to be worth more ~regardless of what the NOI is at the property

Note that in the vast majority of cases cap rates are not within the GPs control and are simply a macro factor that needs to be considered when doing diligence on an investment.

I advise LPs on deals full time and when I give feedback on deals with cap rate compression, I always tell the LP “there’s nothing wrong with investing in a cap rate compression deal as long as:

You know that there is a cap rate compression assumption in the deal (you’d be surprised how many LPs don’t know and assume the GP would tell them)

You understand its implications on your returns, and

You understand that you’re (indirectly) investing into a macro thesis rather than a pure real estate play

It goes without saying that a cap rate needs to be assumed for an exit - otherwise you can’t calculate an IRR! However, from a risk perspective, there’s a big difference between a 2x projected multiple with cap rate compression and a 2x without.

There’s a big difference between a 2x projected multiple with cap rate compression and a 2x without

So if cap rate compressions are outside the control of the GP, why would they assume them?

Because the returns will look great!

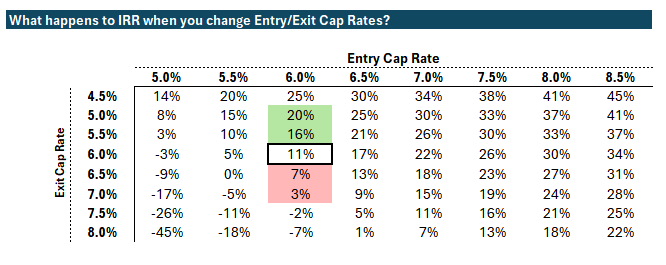

Take a look at the below table (see why most LP investments won’t 2x your money for the full article & assumptions).

If you start at the 11% square and move up to where the green is, you’ll see that lowering your exit cap rate by 1% (100 bps - from 6% to 5%) moves the IRR you present to investors from 11% to 20%.

Now, let’s run through some examples because I want to illustrate two separate points:

Example 1: Cap Rate Compression Saving a Poorly Operated Deal

The Deal: A GP acquires a multifamily property at a market cap rate of 6% with $100,000 in NOI equating to a purchase price of $1.66MM.

Operational Failures: The GP struggles with management, and expenses rise due to maintenance and operational inefficiencies. NOI drops to $75,000, in part due to vacancy, increased costs, and delinquency issues.

Cap Rate Compression: External market factors cause cap rates in the area to drop from 6% to 4%.

Sale: The GP sells the property for $75,000/4% = $1.88MM and, ignoring fees, records a 1.66x = (1.88-1.66*.8)/(1.66*.2) multiple at the deal level assuming the original acquisition had 80% leverage.

The Lesson: While LPs received a return and there’s reason to celebrate on both sides, it’s important to understand that the returns weren’t a result of the the GP’s efforts.

The reliance on cap rate compression masked the GP’s poor operational performance, which is certainly something you’d like to know about a GP’s track record (see more in #2 of Track Record Audit)

Example 2: How Overpaying for a Property Can Make Cap Rate Compression Misleading

Deal: A GP purchases a property at a 4.5% cap rate, but the true market cap rate for similar assets is closer to 5.5%.

Perception: On paper, the GP presents the deal with a projected exit cap rate of 4.75%, which seems reasonable compared to the 4.5% going-in cap rate. In fact, it might even seem conservative - it has cap rate expansion one might conclude!

Reality: The 4.75% exit has 75 bps of cap rate compression embedded in it, since the market rate cap rate was actually 5.5%.

Lesson: Overpaying for a property at an artificially low cap rate relative to market might conceal a cap rate compression (on top of the overall risk of overpaying).

So, you might (rightfully) ask - great, but how do I figure out if the GP is overpaying?

The answer to this is doing a lot of due diligence on market comps - I will write on that more in the future. For now I’ll just say that you certainly shouldn’t invest in a property where a proper comp set wasn’t shared with you.

If you still have energy to read more, I would also recommend reading more about the cap rate compression’s cousin - the refinance assumption trap.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos in 4 weeks together with me and other LPs to learn how to find good LP investments.

LP Topics Seminar** - **an ongoing biweekly 1 hour meeting with other LPs where we'll go over investment decks, capital calls, distressed situations, and modeling. This is meant to provide a deeper look into existing LP investments. Please reply to this email if you’re interested.

***LP Community - ***free 2,500+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can reach me at aleksey@hey.com.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.