Aleksey Chernobelskiy

•March 15, 2024

Why LP investments won't let you quit your 9-5

A monte carlo analysis on the most famous syndicator marketing method

*Welcome to the **31 *subscribers who joined since the last issue!

Last premium post: Single tenant net lease syndications

Last free post: LP Investing Digest #20

**

If you just joined:** I write twice per week and you’ll receive those emails as I post them. One article is always premium (such as this one), while the other is a free weekly digest on LP topics that might be helpful to you. If you’d like to upgrade to premium (which includes access to full archive of my articles), you can do so here:

Why LP investments won't let you quit your 9-5

As I peruse websites and LinkedIn pages of syndications, I continue to see the “quit your 9 to 5” narrative. I recently even saw it written as “grind to five”… which honestly just reminded me to write this article - welcome back! 😊

Today I’m going to try to explain, using a model, why these marketing messages are -at best - misleading.

I’ve been outspoken about this in the past (screenshot below), and I know many don’t like it.. but I’m here to show my work and will obviously take any and all criticism as always - in fact here’s a link to post your refutation! :)

Today's agenda:

What is a monte carlo simulation?

Why is it relevant to LP investing?

Assumptions

Discussing the results

Takeaways

Let’s dive in.

1) What is a monte carlo simulation?

I mean, first of all, what in the world is a monte carlo simulation?! Good question.

Simply said, a monte carlo simulation is where you start at a given point, assume some things about what happens along the way, and see where you end up! The result looks something like this (a random picture I found on Google).

You’ll notice that everything starts in the same spot… and then the result vary quite a bit depending on what happens probabilistically at each step of the model

One easy way to think about this is coin flips:

Take 50 people, and give them 100 coins each

Heads means they win a dollar, tails means they don’t make anything

You can imagine a chart of outcomes in your head:

Each person would have somewhere between $0 and $100 dollars..

All 50 people started at $0 and the outcomes will vary

Ok, cool… but why is this relevant to us? 😊

2) Why is it relevant to LP investing?

Monte carlo simulations are relevant to LP investing because outcomes (even with the best due diligence) will vary … and to add to that, they’re generally outside of your control after you invest. This is why I always say that the best passive investments take active work in the beginning.

The best passive investments take active work in the beginning

Most (all?) of the websites and ads that preach this “passive income to quit your 9-5” story want you to think that investing in syndications will lead you to retirement .. and the question I have is whether that’s actually true!

3) Assumptions

Recall that our goal is to figure out whether “investing as an LP will help me quit my 9-5..”

Let’s subdivide the “population” into 3 categories:

“Very wealthy”

If someone already has the cash saved up to retire through dividends in the stock market (or investing in bonds, treasuries, etc), investing in LP investments doesn’t change the fact that they can retire.

Therefore, this can’t be the case these websites are speaking of, since the individual is already ready to retire!

QED (that’s short for a proof being over, sorry to bring you into my math major nightmares haha)

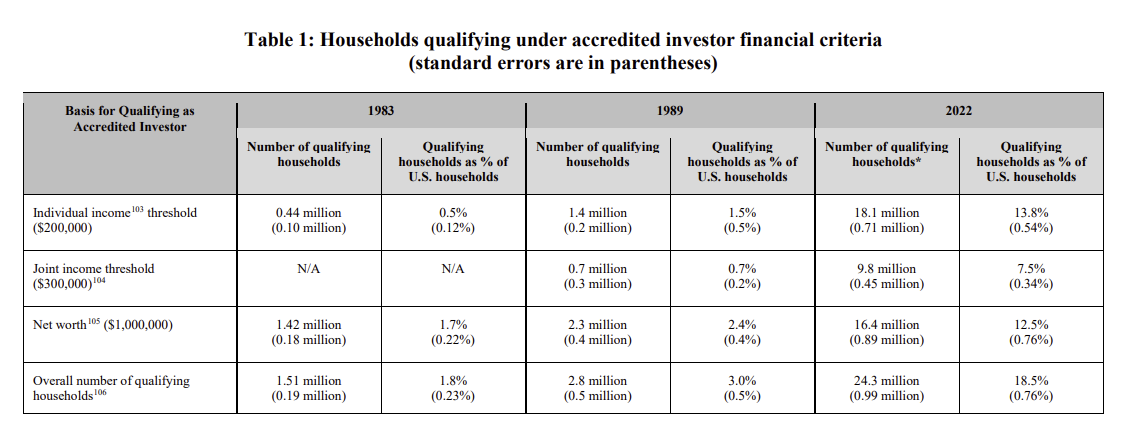

“Accredited”

This is the section we’ll be dealing with in the analysis below

Note that the accredited world is large - roughly 18.5% of US households (which includes the “very wealthy” group above as well)

Nobody, in my opinion, should put all of their investments into one strategy (with the only exception being a business they’re running perhaps, but that’s not our topic)

Therefore, it’s important to allocate only a certain percentage to LP investments - which is the case we’ll deal with in this article!

We will assume $100k below

“Non-accredited”

Both 506(b) and Reg CF (regulation crowdfunding) investments allow investors that aren’t accredited

There’s a lot to say on this, but for the sake of simplicity let’s remember that this is ~81.5% of the US population and I would argue one of these will always be true:

Investor doesn’t know how to vet LP investments (ie loss probability is high)

I would also argue that for many people that fall into this bucket investing the capital into themselves (e.g. education) or using the time they would spend on vetting these deals on advancing their career would probabilistically yield higher returns in dollar terms over a long horizon

Investor doesn’t have enough saved up to make a material dent in saving towards retirement (e.g. if you want to invest 10% of your net worth into syndications a 100k check would already put you into the 1MM net worth bucket that we talked about in 3 above

There are some edge cases here, but I think you’ll agree after reading this that we’ll deal them via #3’s case

To be absolutely clear, where I stand here here is that for a non-accredited investor it’s very unlikely that these outcomes will lead to helping you retire

QED again :)

One path is over allocating and “risking it all,” but I hope we can all agree that’s called luck rather than investing)

One path is over allocating and “risking it all,” but I hope we can all agree that’s called luck rather than investing

Alright, so now let’s get to the fun parts - the modeling!

**PS if you’re still reading… you’re in the 1% of nerdy LPs, perhaps an “accredited LP nerd” would be proper!? **🤓

4) Discussing the results

First, let me introduce you to the uniform distribution- this is basically where you pick any number at random between two numbers.

In our case, I chose 0 to 1. The number on one draw could be 0.9999, 1, or perhaps 0.11111. I hope that makes sense.

We will use this variable to determine what happens to someone’s money after a 5 year period (which is a typical hold period in a syndication). Then we’ll use it again to see what happens in the next 5 year period… for a total of 40 years.

Now, one clear problem is that a multiple between 0x and 1x is clearly unfair - nobody invests in those odds, right?! You’re right, so we’re going to adjust it 3x whatever the number generator gives out.. in other words, pick a number a between 0 and 1, and then multiply by 3. This accounts for the fact that some syndications will have outlier results, while others might lead you to lose your money (but recall that our original draw of 0.5x, a loss, will now be 1.5x .. so the odds have moved!)

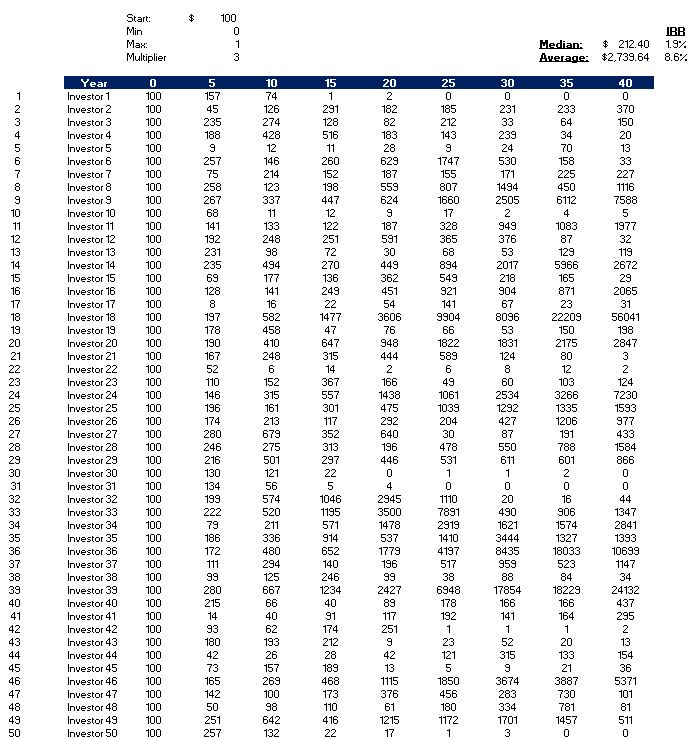

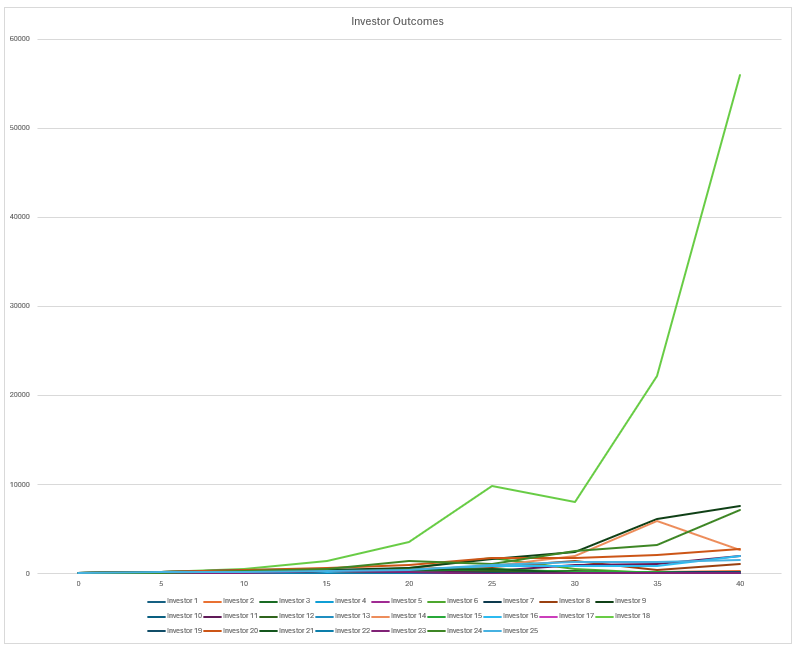

Here are the results:

We start with $100 (for the sake of our example, let’s assume that’s thousands)

Two examples based on the table below:

Investor 3 did well on their first deal - a 2.35x multiple in 5 years, and teh second one was alright, but then the third one (a random number generator again) didn’t do so well… the experiment continues on until the investors ends up with 150 (vs original 100) at the end of 40 (!) years

Investor 18 absolutely crushes it - $56 million from a $100k check!

Over a 40 year period, the average IRR with this simulation is 8.6%, where you’ll end up with $2.7 million (and you started at 100k, pretty cool!)

Let’s remember that there’s inflation… we’re ignoring that

But remember that averages are skewed by outliers.. and $56 million from above is quite the outlier… so now look at the median… roughly a 2x multiple over a 40 year period, or a 1.9% IRR - ouch!

Here’s a graphical representation of the first 25 (50 gets a bit busy):

A fair question on the above methodology is “but outcomes shouldn’t be equally spread between 0 and 3x. For example, it’s more likely (across a large enough sample size) to get all your money back in a real estate syndication vs losing it all.

You might even imagine a normal distribution (a bell curve), but the problem is that this curve has no bounds (while with an LP investment, the “worst” outcome is losing it all as opposed to losing more than what you had). I have a few ideas for the right distributions for this and will do part 2 soon for the ultimate accredited LP nerds - stay tuned!

5) Takeaways

I think there are a few lessons we can take away from our work today:

Accuracy matters - you can see how expensive it is to lose money, in some cases our investors couldn’t recover from the loss in a very long time horizon. More on that here

Secondly, and not including inflation, your $100k check (on average) will get you to $2.7MM on average… but only $212k using a median (here the median matters more, since it’s an actual outcome, as opposed to the average)

Even the average IRR of 8.6% isn’t so incredible… and the entire time you didn’t have liquidity like you would in the stock market (which also averages 8% over a long hold period)

Having said all that, $2.5MM*~8% is a nice $200k check every year while still having your equity invested … and this doesn’t account for additional investments that you might have invested in along the way!

I hope this helps you conclude initially (more to come with another probability distribution) that investing as an LP will only help one (of our three populations of people described in the assumptions section) get to retirement (1) AFTER 40 years (!) and (2) with an investment return that doesn’t differ greatly from a stock market index.

But to be clear this subset (accredited investors) of the population accounts for roughly 18.5%.. while the websites target much more than this..

Perhaps one could even argue that within the subset of 18.5% of accredited investors, there are people who are so inexperienced (recall that accuracy matters) at investing that the entire argument falls apart altogether

Again, more coming on this with a new distribution, where I hope to also show how much accuracy of your investments matter.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments.

***LP Community - ***free 1,800+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can set up an initial consultation.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.