Aleksey Chernobelskiy

•February 7, 2024

5 ways in which real estate can lose you money

Real estate SHOULD be safe, but here's how that logic falls apart

*Welcome to the **98 *subscribers and 10 premium subscribers who joined since the last issue!

Last premium posts: My deal is distressed, now what? & Is my investment distressed? (a 2 week series)

Last free post: LP Investing Digest #15

Announcements:

**Referral reminder: **if you’re on a budget, you can get up to 6 months for free of these articles by inviting 6 friends to this publication!

If you just joined: I write twice per week and you’ll receive those emails as I post them. One article is always premium (such as this one), while the other is a free weekly digest on LP topics that might be helpful to you. If you’d like to upgrade to premium (which includes access to full archive of my articles), you can do so here:

5 ways in which real estate can lose you money

Welcome back! 👋

Over the course of my new venture I've heard an endless number of comments from LPs that sound like one of the following:

“This investment feels safe, but I just wanted to get your thoughts”

“Worst possible case here seems to be that I get my money back”

“Real estate is an asset, so worst case scenario is we can just sell it”

“This investment has to be safe because everyone needs a place to live”

“The GP said the investment returns are guaranteed”

I hear from LPs that have lost a substantial amount of net worth in an investment and they tell me that, at the time of investing, they had preconceived notions that were similar to one of the above comments. I hope that the majority of you can read each one of the above and understand why the reasoning in each statement is faulty at best and perhaps dangerous at worst.

As I discussed in detail in my earlier post below on the investor’s mindset, a healthy dose of skepticism is critical to any investor … and I hope you can use the above examples to practice this. Simply ask yourself, what could go wrong? What’s a counter example.

Hint: if you can’t find a counterexample for an assumption or statement, you probably don’t understand the topic well enough and should be careful making an investment.

Today, I'd like to quickly give you feedback on the five comments above while also providing you with a detailed list on of the top 5 reasons a commercial real estate deal can lose money:

Deconstructing the 5 misconceptions

Top 5 ways to lose money in a real estate deal

**1) **Deconstructing the 5 misconceptions

First, here are some simple counterexamples (which I hope you tried to arrive at on your own):

“This investment feels safe, but I just wanted to get your thoughts”

The only investment that should be called safe is treasuries, and even that (according to some) has a tiny chance of defaulting at some point.

Going into any investment thinking it’s safe is generally not a great place to start.. the risk reward might make sense, but that’s vastly different than calling the investment safe. I wrote about this at length below and recommend you reading this before you continue.

“Worst possible case here seems to be that I get my money back”

Any (yes, any) equity investment has a downside of losing your entire principal unless it’s hedged by some other instrument. I’m not going to get into hedging because it’s not relevant for our discussion today.

You might say that the probability of that happening (losing your equity) is low, but the chance is still there - that is, you CAN actually lose everything.. and therefore the worst possible case is NOT getting your money back, but rather losing it all.

“Real estate is an asset, so worst case scenario is we can just sell it”

The first and second parts here are true - real estate is indeed an asset and (within some time due to its inherent illiquidity) you can just sell it if you’d like

Having said that, you (1) never want to be a forced seller (more on that in the spotting distress section below) and perhaps even more importantly (2) just because you can sell, doesn’t mean you’ll sell at a price that’ll net you your money back (or any of your LP investment back, for that matter).

“This investment has to be safe because everyone needs a place to live”

Everyone does need a place to live, but that doesn’t materially drive anything for your investment. Rents are determined by supply and demand in a given area… surely demand might be there and perhaps it might even grow, but if the supply outpaces demand, rents begin to drop (thereby negatively impacting the investment)

Perhaps even more importantly, this comment ignores true analysis of an investment and pins its merits to what I would call a “feel-good” notion

“The GP said the investment returns are guaranteed”

As I talk about commonly and publicly, nothing in investments is guaranteed and the fact that the deck says that might tell you something else as well - please see #1 here for more on this topic

**2) **Top 5 ways to lose money in a real estate deal

First, let me make something absolutely clear. The fact that we’re discussing this topic means that **you can lose your entire investment on a real estate deal. **Not “just get your money back” and not “I’ll get at least something back,” but rather lose it all - entirely.

I’ve seen this happen and talk to people (nearly) daily that are going through this. Of course, these stories shouldn’t prevent you from investing and they’re not the norm, but they should simply educate you on the fact that losing your money is possible and you should always proceed with caution.

Many people don’t understand the impact of losing money, and I wrote about that here at length - I deeply recommend anyone reading this before making any investment. It takes a very long time to make up for lost principal and that’s the single biggest reason why due diligence is important. If you don’t have time to do it, don’t invest.

Secondly, there is a reason why “Property” is Pillar number 3 (of 3, in order of importance) in my Three Pillars to LP Investing methodology. The first pillar is Execution (your diligence on the GP itself), and the second is Alignment of Interests (between LP and GP). Most of what we’ll be discussing below addresses points within the Property category, but many losses actually occur due to lack of LP doing proper diligence in the first two pillars. Here are the three pillars again if you’d like to take a glance:

Execution - track record and counterparty risk

Alignment of Interests - coinvest, waterfall, and fees

**Property **- valuation and business plan

Finally, let’s remember that (at it’s most basic level) a property’s valuation is the property’s NOI divided by the cap rate. We have 3 separate variables here that I’ll dig into below (Income, Expenses, Cap Rates), while mentioning two others: Capital Structure and External Circumstances

Income

While income is something a GP can influence (via renovating, for example) it’s also important to note that a lot of it is simply market driven. In other words, a GP can charge whatever they’d like.. but if the demand isn’t there they’ll be forced to deal with vacancy or have to lower their rates .. this is why market research at the outset is super important

Once we’re on the topic of vacancy, I want to highlight a few things:

Vacancy has to increase during a heavy construction period… this causes a cash strain on the property that (hopefully) was expected and planned for

Just because you leased a unit at your expected proforma rents, doesn’t mean that you’re out of the woods:

if a 3 month free rent concession was given to that tenant, the effective rents are actually 25% (3/12) below what you expected them to be

you’re not collecting any cash in that first 3 month period

in month 4, the tenant might default and you’ll have to pay money to get them out!

Delinquency is often confused with vacancy and they’re very different things:

An apartment can be 100% occupied (i.e. no vacancy), but only 50% of the tenants are paying (i.e. high delinquency rate).

The delinquency is typically driven by a mix of operational issues (that are within the GPs control) and, at times, government legislation (that generally can’t be controlled or changed materially by a given GP)

Other income (cable, WiFi, water filters) is a common plan in value add projects and I just want to remind everyone that all in cost is what matters many times - in a class C price sensitive demographic you can’t expect to (1) bring rents to the top of market AND (2) introduce a ton of expenses on top of that. Having said that, these plans do work if they’re executed well.

Expenses

A quick disclaimer: It’s generally easy to assume you can run a property cheaper than the prior operator, but sometimes GPs are surprised at what they find once they arrive - the labor pool might be very tough, or perhaps cutting costs right now (even if possible) is suboptimal for other reasons. That’s not to say it’s impossible to cut costs in year one .. I just think it’s very hard to do in practice (even if you assume no inflationary pressures) without having risks elsewhere on the investment

Property Taxes generally go up, and many times they’re also reassessed specially at purchase.. it’s prudent to make sure a significant jump in these costs are accounted for

Insurance costs are on the rise, particularly in coastal markets that have natural disaster risk. Some of these costs have climbed to levels that are unsustainable today and I suspect that some of the foreclosures that we’ll see this year will have insurance costs be a top two catalyst of foreclosure.

Property management mistakes are very common… many firms want to manage internally, but the truth is that both from an experience perspective AND even a cost perspective, using third party management is better for the LP.

If a property is being internally managed make sure to ask the GP how much experience they’ve had internally managing properties and why (economically speaking) do they think that’s better from the perspective of an LP (when compared to external management). Many times vertical integration sounds a lot better than it is (of course with size and experience it starts to make more economic sense).

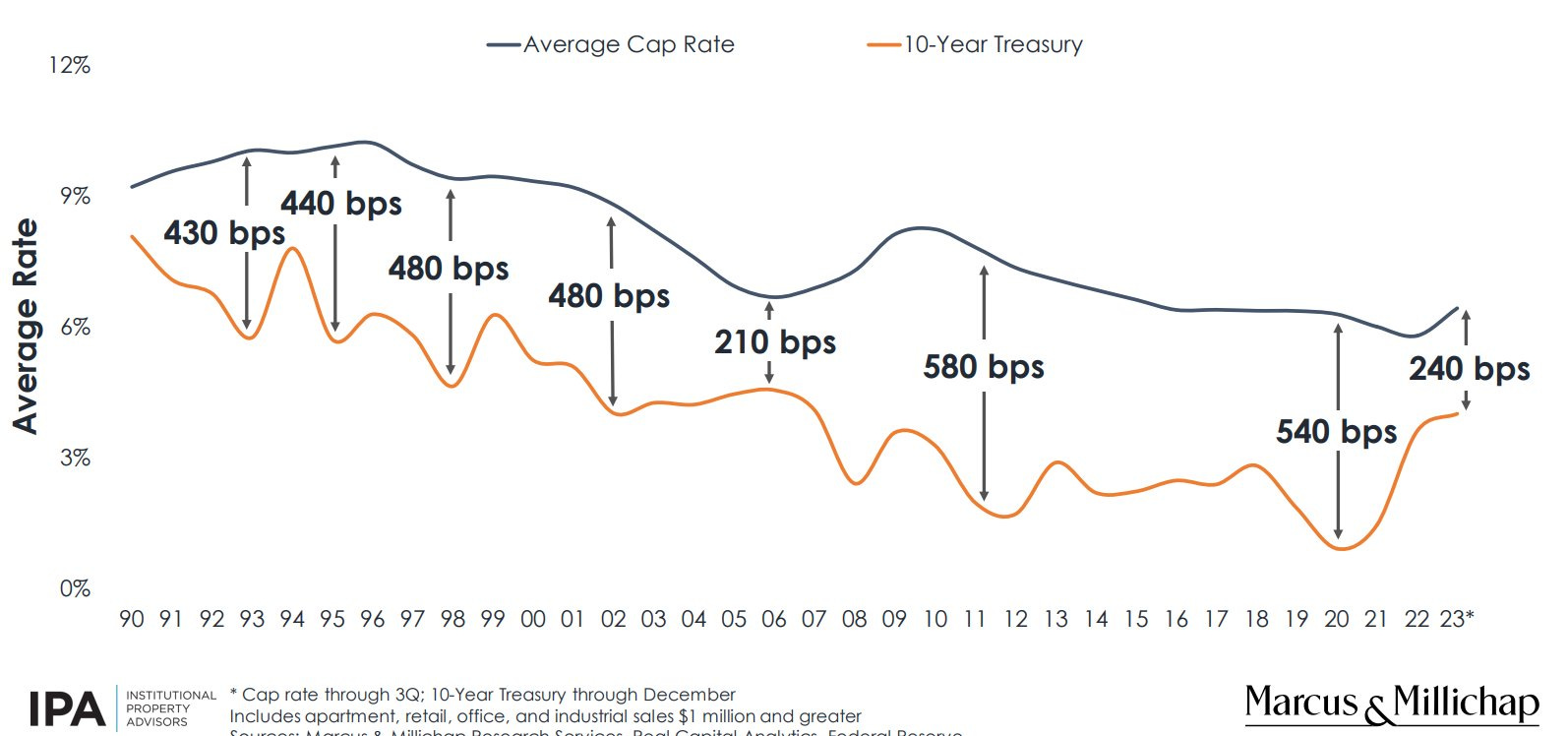

Cap Rates

Cap rates (unless changing from one asset type to another, or going from deep distress to stabilized, etc) can’t be influenced by a GP.. and therefore the exit cap rate is a macro bet that needs to be made very carefully… I’m leaving a chart on this below

The biggest point here is that markets have cycles.. they’re generally very hard to predict even for the best investors, so instead I would recommend the following:

Instead of focusing on what will happen, make sure the investment can sustain itself (i.e. you’ll get your investment back, let’s say) if cap rates move in the wrong direction (recommend a similar exercise for any major variable that has a material impact on your investment)

Remember that most LP syndications are made in short time horizons, so although there are a lot of great “downward” pressure time horizons in the image below, the key is to not get stuck in a short term vehicle (where the debt pressures you to make a decision, for example) on the way up

Capital Structure

Forced sales are never good, because you might be forced to sell earlier than you’d like to (as equity you always want the option to sell when you’d like.. rather than being told to do so) .. a forced sale can (officially) can from ANY partner in your capital stack, which certainly includes any debt obligations or a preferred equity investment.

Debt (and pref equity, rate caps etc) instruments are great tools to increase equity returns, but they always come at a risk… that risk is the fact that at expiration or maturity, something changes (you need to pay more, pay your loan back, raise more cash, etc) .. and that something might force you in a decision that you don’t want to make at that particular time

Expenses only matter in the sense that they need to be covered by income during that period. To the extent that expenses rise to level that's not sustainable (and assuming there weren’t capital reserves to meet these needs), the property immediately goes into a challenging state … which could ultimately lead to a forced sale. Although both capital expenditures and debt service are both below the line (i.e. typically not counted in NOI), it’s important to note that they can have big implications:

The biggest one is that the NOI produced by the property needs to be able to cover debt service.. and of course the debt service might increase over time (as a result of amortization kicking in after an interest only period, a rate cap expiring, or simply a floating rate loan)

It’s also important to note that although debt service isn’t part of the “regular” NOI/Cap Rate valuation calculation, there’s no question that debt service costs impact one’s willingness to buy a property… which thereby impacts the property value as well. Said another way - keeping other things constant - rising interest rates decreases the demand of asset heavy investments, since the return you’re able to receive on such an investment no longer compensates you well enough to take on the risk.

This should be thought of “proforma” debt costs… i.e. just because the current owner has cheap financing on a property, doesn’t mean the buyer could get the same thing (i.e. the loan isn’t assumable by the incoming buyer).

As a tiny tangential point, the same is true across revenue and expense assumptions at large - the buyer might say your income is overstated (accrual accounting vs cash) and your expenses were understated (expecting a large increase in property taxes or insurance, as one example).. this proforma change will impact the NOI the buyer is using to value the investment.

On capital expenditures, reserves are critical because they function as working capital. In order to fix up a commercial space, you will typically pay up front for the improvements, and then ask the lender for a reimbursement.. sometimes the reimbursement process takes months and other times some items might not get reimbursed at all. Due to this, a cash crunch period might leave you with unfinished units that can’t be rented out and can’t be finished either.

Needless to say, having a good understanding of cap ex needs ($ necessary to get to your goal) is critical here ... some inexperienced operators make guesses that are very deeply below true construction estimates and this impacts the project

External Circumstances

I’m not going to go into an entire list of ways to lose your investment in this section because a lot of it is not in the control of a GP

However, insuring properly for some of this is VERY much in the GPs control .. and I have heard stories about GPs (due to costs) cutting corners on insurance - needless to say, this is a risky bet that can be diametrically opposed to the GPs fiduciary due to their LPs

Regulation is a big one that’s not discussed often.. the ability to evict a non paying resident (and rent control measures in general), for example, is a law and it can be changed at any point. Such a change impacts the current owners ability to operate, but also changes the perception of the investment thesis for an incoming buyer.

Environmental issues that come up after buying (the new owner would be forced to remediate)

For an additional discussion on this topic, see here and here.

Thank you for reading! I genuinely hope you found this helpful - the best way to say thank you is to spread the word.

I have dozens of topics on my list for 2024 and I’m very excited. If you have a topic you’d like me to cover or have any questions on this article, please leave a comment.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments.

***LP Community - ***free 1,700+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can set up an initial consultation.

Limited Partner (LP) Investing Lessons is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.