Aleksey Chernobelskiy

•January 30, 2025

Criss-cross rescue sauce

On the implications of crossed LLCs for LPs

Welcome back and happy Wednesday!

I’ve been posting for a few months (most recent post below) about the fact that GPs are crossing single asset LLCs in order to attract rescue capital, and now it’s finally time to dig in.

Today we’ll cover:

Simple definitions

An example using Preferred Equity

Negative implications to LPs and how to spot these situations

Advanced versions of this tactic

To set the stage, we’re talking about an event that typically occurs during distress. As I wrote (screenshot below) in my 2025 predictions, I expect this phenomenon to accelerate this year.

Announcements (article continued below):

**March LP Cohort: **Review 4 deals with me and a small group of other LPs to learn what to look out for in deals. Please reply to this email if it’s of interest.

**GP-LP Match is live and deals are going out daily that match your criteria for free! **If you’re an LP or GP join here in under a minute. I’m behind on verification for LPs so please ping me privately to expedite once you sign up.

**Last premium post: **10 reasons why deal flow rules the world - why seeing more deals is better for serious LPs

Simple definitions

A single asset LLC is an entity that holds a single asset, such as a property. The property was purchased using GP and LP equity, alongside other capital partners’ cash (e.g. debt).

Crossing assets means that you’re being signed up for risk that you originally didn’t sign up for - that simple. More below in the example and it’ll become a lot more clear as we go through this

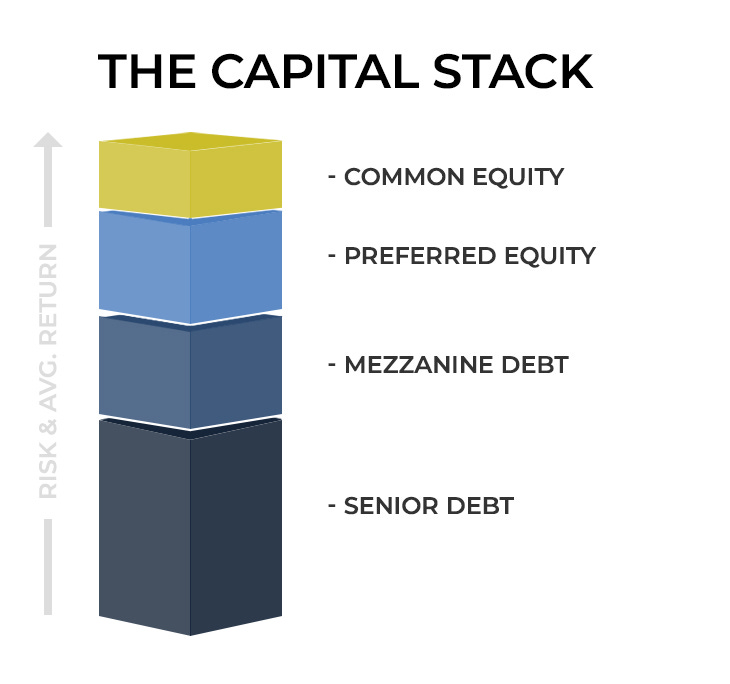

Here’s a simple illustration of the types of instruments that exist within a given capital stack - in other words, a single LLC could have ALL of these parties at once (it’s most common to close on an asset with just debt and equity, but this should never be assumed)

When an asset is sold, senior debt gets paid in full first, then it goes to mezz … and so on. Once you get to common equity, that’s where the GP/LP waterfall kicks in

An example using Preferred Equity

Assumptions:

LP_1 invests in Deal_1 holding a single property

LP_2, a different person, invests in Deal_2 holding a totally different property

Both LP_1 and LP_2 invested in single property LLCs instead of a fund because they did their diligence and were comfortable with the asset - if their respective asset performs well, the individual LPs will get great returns .. and vice versa

The GP behind Deal_1 and Deal_2 is the same GP

Trouble strikes

Fast forward some time since acquisition

Deal_1 has a major capital need and the equity is wiped out

Capital need could be due to lack of cash flow, or could be due to debt maturity / rate cap expiration

Equity wiped out means if you invested $100k, it’s worth nothing today if the property were to be sold .. a few explanations for how this could happen can be found in 5 ways in which real estate can lose you money

Deal_2, on the other hand is doing alright.. perhaps not amazing, but alright! For the sake of example let’s assume the equity is worth 1.3x of what you invested

In other words, if you invested $100k, the equity is worth $130k if the property were to be sold today

GP reacts

Running out of options on Deal_1 (step 1 is typically a capital call, which you can read about below), the GP gets a call from an investor interested in investing through Preferred Equity

But there’s a problem - the only property that needs help, Deal_1, is worth the amount of the senior debt on the property (or in some cases less) - this has to be true, since the equity on the property is worth nothing

So, the investor offers to provide Preferred Equity across both Deal_1 and Deal_2

The problem

Since the Preferred Equity investor’s collateral is both Deal_1 and Deal_2, you can probably see how this can go haywire - simply said, the worse the performance of Deal_1 the more the investor will expect Deal_2 to compensate in a downside scenario

As a reminder - the preferred equity investor needs to make their money.. otherwise (as we saw above in the capital stack graph) the common gets $0

So, to summarize:

If you’re an investor in Deal_1, you’re excited.. you just got another lifeline!

If you’re an investor in Deal_2, you’re not happy - this isn’t what you signed up for - you simply want your 1.3x return and don’t want the return to be tied to anything else (that’s what you signed up for… right?!)

You can also change Deal_1 and Deal_2 to being worth 0.5x and 1.3x and see how this would work in a similar way

If you’ve made it all the way here, it’s time for a meme 😊

Negative implications to LPs and how to spot these situations

Most times these situations happen during distress - see the following to check whether your investment is in distress

In the vast majority of cases, these things also happen when the GP has something to gain from taking the legally complicated (best case) or unethical (middle case) or illegal (worst case) path to raising capital and saving their reputation. You can read more on how to spot misalignment below

To put it bluntly (and I’m not saying these situations are easy) the GP has two options in front of them using our example from above:

The two options are:

Take a total loss on Deal_1

Pursue the Preferred Equity solution

Putting ethics aside (I like to give people the benefit of the doubt, but have seen my fair share of unethical behavior), you can imagine how a GP who doesn’t want to take a total loss on Deal_1 and pursues the second option instead.

Taking a total loss could mean all types of things, including headline risk, having a harder time fundraising equity on new deals, losing lender relationships, etc.

Advanced versions of this tactic:

We’ll get into some more advanced ideas on this topic below, but first let me just say that ALL of these scenarios have (what I would call) edge cases where things are done fairly, but I feel comfortable saying that the majority of these scenarios unproportionally benefit one party (LP_1 in our example above) over the other (LP_2 in our example above)

All - and I mean all - of these strategies will be pitched to you as being good. The most common pitches include diversification benefits, and there are others … but you must proceed with caution because ~most times these sales pitches are only presenting you with the benefits.

Your job is to be skeptical (because that’s not what you signed up for) and make sure you understand the other side of the trade (think: what’s worse for me as a result of these changes relative to what I had before?)

Some common tactics:

Recapitalizations / continuation funds

In our example above, LP_1 and LP_2 are recapitalized into an LLC that holds both assets

Continuation funds are of similar nature - they’re basically set up (in most cases) to avoid selling today (either because it’s not a good time or because equity would lose money thereby impacting the GP’s track **record) **

REITs

LP_1 and LP_2 (and typically many more single level LLLs, or funds) are all rolled up into a single Real Estate Investment Trust (REIT) with common ownership

Pref Equity - as described above

Mezzanine Debt and Debt Refinances

This is similar to the Preferred Equity case, but just another security type (that’s more senior in terms of payment compared to pref)

The concept stays the same - a single lender (or a group of them) come in and take collateral to more than the property that you’re invested in … sometimes this occurs in conjunction with paying off existing LLC lenders.

Thank you so much for reading, I hope this was helpful and look forward to your feedback as always.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

***GP-LP Match - ***a simple way for you to get more deal-flow that matches you precise LP parameters. You can join here in under a minute. I’m behind on verification for LPs so please ping me privately to expedite once you sign up.

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos in 4 weeks together with me and other LPs to learn how to find good LP investments.

LP Topics Seminar** - **an ongoing biweekly 1 hour meeting with other LPs where we'll go over investment decks, capital calls, distressed situations, and modeling. This is meant to provide a deeper look into existing LP investments. Please reply to this email if you’re interested.

***LP Community - ***free 2,800+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can reach me at aleksey@hey.com.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.