Aleksey Chernobelskiy

•December 21, 2023

Is real estate better than treasuries?

Why "investing in treasuries" is an overused yet helpful real estate comp

*Welcome to the **109 *subscribers and 6 new premium subscribers who joined since the last issue!

Last premium post: Hidden risks of tax benefits in syndications

Last free posts: top 15 syndication mistakes and LP Investing Digest #8

Announcements:

🎁 **New Year’s GP Special: **if you’re a GP and would like to gift 3 months of premium articles to your LPs for the holidays at no cost to both of you, please reply to this email. If you’re an LP and want to forward this email to your GP, even better!

🎉 **December promotion: **earn a free month of premium for every friend you refer to this blog. Click the button below to get started. Many people just took this link and sent it to a group (e.g. Facebook, Whatsapp, etc) that they’re on with other likeminded investors.

Why "investing in treasuries" is an overused yet helpful real estate comp

You’ll hear many people (TV, Twitter, YouTube, etc) say things similar to “why would I buy a 4% cap if treasuries are 5%?!”

Today I’d like to build an investments framework and explain that, while these cap rate to treasury comparisons are usually misinformed, treasuries do carry a significance in the investment landscape that shouldn’t be ignored.

Here’s our agenda for today:

Three simple investment rules

**Main differences between real estate and treasuries **

Expected values applied to real estate investing

Ok fine, but “why would I buy a 4% cap if treasuries are 5%”

First, let’s begin by painting the landscape of investments in general. As a reminder, everything we speak about are just my thoughts and are not investment advice.

Real estate’s upside is great, but it is somewhat capped in probability, so saying no to an investment is critical when you think that the downside risk on your investment is more than you can bear. Expecting real estate to provide you venture capital type returns is (in probability) a really bad idea. Similarly, going into a VC investment thinking it's safe is a bad idea. Real estate returns aren’t literally capped (since equity returns don’t have a real ceiling), but rather "capped in probability" from the investor’s perspective. We’ll touch more on this soon.

Said another way, if someone is investing in a stock index expecting to make a consistent 20% per year, I think we would all agree that doesn’t make sense (stock market returns tend to be in the 7-10% range).

Can someone make 20% in a given year? Sure... but "in probability" stock market index upside is capped in the same way that I think real estate upside should be thought of. Doubling your money every 5 years (15% IRR) is a phenomenal outcome in real estate ... can you do better on a given deal? Yes, but did you get lucky due to variables that were outside of your control (and outside the true investment thesis)? I would argue that in most cases, the answer to this is also yes.

In my mind, “success” as an investor is entering an investment (regardless of its risk level) with a good understanding of the risks involved. The opposite is also true - I have a really hard time with people investing blindly, which is why you shouldn’t be investing $5,000 into syndications.

1. Three simple investment rules

If you don’t have time (or curiosity) to learn to invest, don’t invest

If you’re not willing to put in the effort to look at many deals to invest in only one (through proper due diligence), don’t invest

For more on an investor’s mindset, see here.

Finally, from a book on Naval’s thoughts (this Twitter thread is a great free summary): if you can’t decide on investing, the answer is no .. plain and simple.

From my work, I’ve come to realize that many take on risk with a return profile that is subpar relative to the risk that they are taking on. Let me provide an example.

Today we are living in incredible times - you can invest virtually any (beyond $250k isn’t FDIC insured) amount of money in a savings account, earn well beyond 4% (Marcus below is 4.5% for example) and have no penalties for pulling it out. If you put some of your savings into an account like Marcus (many of these out there, but screenshot below as an example), the money is available to you at any point (as long as it’s short term in nature … e.g. if you buy a 3 year bond, you’ll have wait to maturity to get your money back or might have price fluctuations depending on where interests rates are at any given point during your hold period).

This should be part of any investment strategy as an LP - the “floor” of your assessment of the investment proposal. In other words, the baseline option is always “do nothing and earn 4-5% risk free” and have it be liquid to you once you find a great opportunity. This comes with two caveats:

There’s a chance that these high savings rates won’t last (if the fed cut rates), and

Of course you’d rather have your cash compounding at much higher rates than 4-5%, but this is always a function of risk that you’re willing to take to “access” those higher returns

The baseline option is always “do nothing and earn 4-5% risk free” and have it be liquid to you once you find a great opportunity.

So, how do treasuries (or these liquid savings accounts) compare to syndications?

2. Main differences between real estate and treasuries

- The first difference is the fact that you are a silent partner and have no say in the investment post investment

This is important and requires a lot of trust, since people act differently depending on incentive structures. This is why Execution (the first LP investing pillar that includes trust) and Alignment of Interests (the second LP investing pillar that deals with incentives) come **before **getting to the third pillar - analyzing the actual property.

For instance, the fund might be underwater (i.e. the GP entity itself isn’t healthy) and in desperate need to bring in a fee in order to pay salaries at the general partnership. In order to bring a fee, they might be “forced” to buy a deal or sell an existing deal, in order to cover payroll. In such circumstances, you can clearly see how the GP is misaligned to their existing and/or future LPs.

- The second difference is liquidity.

Liquidity is very important as you might need the cash that you invested at some point whether it be for personal needs or another phenomenal investment opportunity that comes up.

Oftentimes, even though the life of a deal in a PPM might be stated as 5 years, the reality is that the life of a fund (or a deal) could last longer as a result of a GPs’ decision to keep an asset, which, as described above in #1, might be in direct conflict of interest.

As a result, you should be compensated for the additional risk of not having liquidity when you might need it for a another transaction (an LP position, generally, is illiquid - you can’t sell it).

- The third is the risk of the deal itself, putting the sponsor aside

Even if you trust the sponsor and think the incentives are aligned (#1 above), and feel that you’re being compensated well for the illiquid nature of the investment (#2 above), there’s still the inherent deal of the property itself.

The asset itself, how the asset is capitalized, and many more factors are at play here as I discussed in depth in the third pillar.

3. Expected values applied to real estate investing

Although investment decisions are binary (i.e. you either get your money back or you don't, you double your money or you don't) I personally like to think of investments from the perspective of expected value.

In the case of investing in treasuries, you have 100% chance of making 4-5% with great liquidity. It is essential to compare from the perspective of probabilities what you're expected value outcome would be when investing in something else. Expected value does not account for the liquidity aspect (i.e. having the money available at any point for a financial need or better opportunity) and discount rates (i.e. time value of money - how long one investment takes over another). Both of these aspects should weaken the prospect of putting your money elsewhere, directionally … but the question is when does it start making sense.

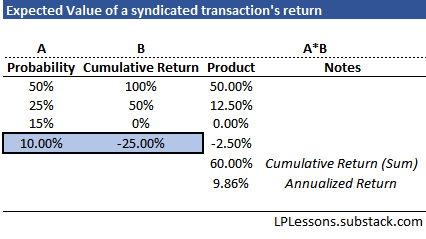

For a simple example, assume you’re looking at a syndication and think that there’s 50% chance of making double your investment (100% return on your investment over 5 year hold), 25% chance of a 50% return (1.5x multiple), 15 % chance of no return (you get your money back), and 10% chance of -25% loss (remember, downside is really important and no investment is risk free).

The outcome would be that you would expect a cumulative return of 60%, or 9.86% annualized:

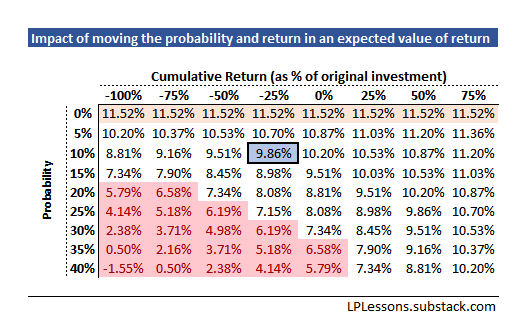

Now you might (correctly) ask - what happens if that 10% probability is different, and perhaps we won’t lose 25% (maybe it’ll be more.. or less).

Let us sensitize the two variables highlighted in blue above (the 50% probability is set to adjust to summing to 100%) to see what happens:

to orient ourselves, find the 9.86% in the table below first - this is the number we just saw above based on a 10% probability of losing 25% of your principal

now notice the 11.52% numbers that are highlighted: when the probability is set to zero on this variable, the cumulative return is irrelevant since the return has zero probability of happening … so that makes sense!

the numbers in red are all below 7%, which is slightly above the risk free (joke here - which you deserve since you’ve read a lot so far!) rate nowadays. I would argue that, based on everything we learned above (illiquid nature of syndications, no control, etc.) it doesn’t make sense to put your money at risk into something that you expect to make less than 7% in probability, because the spread between this and the risk free rate doesn’t compensate for the amount of concentrated risk you’d be taking in this single asset.

Now, with the framework behind us, let’s finish by answering the question from the beginning.

4. Ok fine, but “why would I buy a 4% cap if treasuries are 5%”

Firstly, let’s start with the fact that capitalization rates in real estate are not created equal. In other words, saying “4% cap” can have many different meanings that should get different reactions from an investor. That is not the purpose of this article, although I address this at length in 4 reasons why cap rates are misleading.

Putting the misleading nature of cap rates aside, buying a 4% cap does not mean that the investor is expecting a 4% return. Most investments have a thesis behind them in order to generate a return to the investor that exceeds what one may be able to get in other alternative investments (such as the stock market, or treasuries, in our example).

So chances are, the 4% isn’t representative of the the investments actual return. Using the expected value approach we looked at above, we can probabilistically arrive at the rate of return we expect, and compare it to the risk free rate options available. At that point, the question every investor needs to asks themselves is - is the additional expected return worth the risk?

PS treasuries vs real estate comparisons also ignore the tax benefits behind syndications - but don’t forget the risks too!

Thank you for reading! I genuinely hope you found this helpful - the best way to say thank you is to spread the word.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Wealth Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos together with me and other LPs to learn how to find good LP investments. The January cohort is now full, but the February cohort still has 4 spots available.

***LP Community - ***free 1,400+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can set up an initial consultation.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.