Aleksey Chernobelskiy

•August 15, 2024

Will a rate cut(s) save distressed investments?

Cuts are approaching, but will they actually help?

**Last premium post: **LP Investing Lessons Podcast #6

Last free post: LP Investing Digest #42 & Full Article Index By Topic

Announcements:

**LP Topics Seminar: **an ongoing biweekly 1 hour meeting with other LPs where we'll go over investment decks, capital call and distressed situations, and modeling. This is meant to provide a deeper look into existing LP investments. Please reply to this email if you’re interested.

**LP Cohort: **I have space in the September cohort. Please reply to this email if it’s of interest. Review 4 deals with me (4 consecutive weeks) and other LPs to learn what to look out for in deals. I recommend doing this before the LP Topics Seminar.

Will a rate cut(s) save distressed investments?

Happy Thursday! 👋

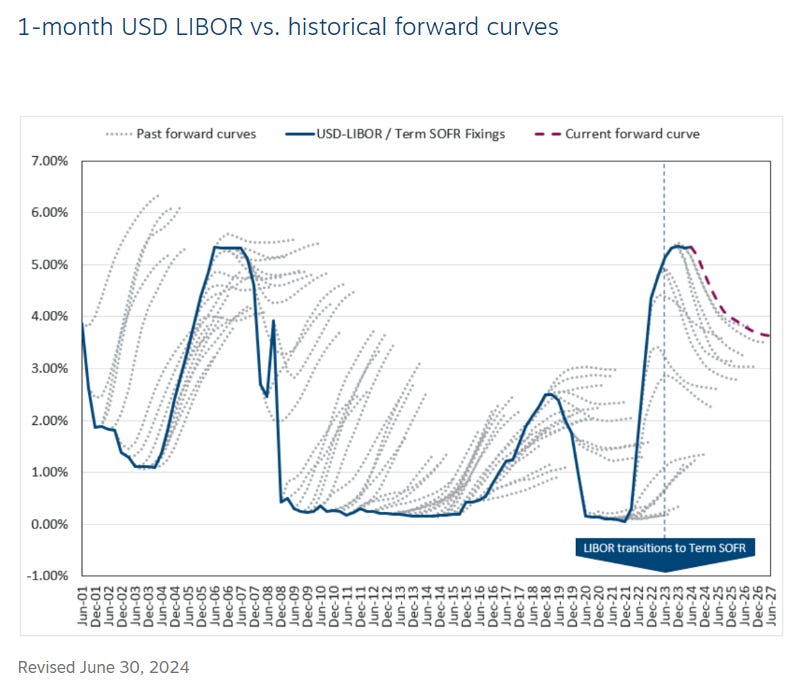

All major headlines seem to be pointing to an upcoming rate cut, which begs the question - will it really help existing investments in distress? My goal today is answer this.

For some background, here’s the front page of the WSJ yesterday:

You can also see below that, from a betting market perspective, investors seem to be pricing in a cut with 95% probability.

While everyone seems to agree that it’ll happen and the argument is around how much (25 vs 50 bps, i.e. 0.25% vs 0.50%), does the change cause the relief many LPs need?

First, let’s define distress to hone in on a specific case.

For the sake of simplicity, let’s say it’s defined as cases where the equity of an investment is either $0 (i.e. the entire equity investment is wiped out even though the property hasn’t been sold yet, a paper loss) or negative (i.e. investment is worth less than the debt outstanding - believe it or not, I’ve seen many of those). See here for more on identifying distress in an investment and what to do once you’ve identified it.

I’ll preface this discussion (and my opinion that follows) by reminding you that I’m not a macroeconomist. While we’re on that topic, I’ll take the moment to illustrate how even the most educated and smartest macroeconomists can get predictions wrong [this is why (1) two variable sensitivity tables are so critical when considering any investments - many examples of them here, and (2) I suggest looking for the top catalysts in a deal - see #2 here]:

Alright, so let’s say a rate cut happens.

Here’s what happens next by its impact on real estate:

Cost of Borrowing Decreases

This is likely the most obvious one. Interest rates on commercial mortgages are likely to decrease as a result of the rate cut. This is likely, but I would say it’s also likely the least “helpful” thing in terms of distress.

If you weren’t able to pay your debt service at 7% and you’re on a floating loan, you’d welcome a 6.75% rate but the change won’t save the deal where the equity is wiped out

Cost of Rate Caps Decrease

This one’s a bit more promising, I think, because many distressed deals (or ones that are on the cusp of distress) are on floating rate loans with rate cap expiring

For some background, rate caps are bought with the premise that if rates go up, your borrowing rate on the mortgage will be “capped” at a ceiling.

This is effectively a hedge on rates going up.. and as rates start coming down, you could certainly see the price of such instruments drop.

This means that anyone who’s expecting to need to purchase a rate cap (because they can’t afford the floating rate as is or want to hedge rates rising) might be able to get one for cheaper than they initially expected.

But remember – we defined distress as scenarios where equity is wiped out.. and although a rate cap might come marginally cheaper as a result of cut(s) this unfortunately won’t save the deal either.

Sentiment Changes Boost Values

You could certainly see buyers come back to the market once they see some stability in the capital markets. The increased stability might also cause more favorable terms from lenders (e.g. not just lower interest rates as we discussed above, but higher loan to value loans → more proceeds for a buyer to purchase a building).

This is the most meaningful aspect to our discussion today, since it could cause a slow repricing of asset values.

Taken to the extreme for the purpose of an example, if you have an asset that used to be worth $100MM and you borrowed at 3% to buy it (and make sense of buying it through your model/assumptions) and rates start dropping lower & lower, you can certainly see a path to the $100MM number again (or perhaps even higher if NOI has moved up in the interim).

A bit more on this further down below, since there are other variables at play such as rent and expense growth…

What’s interesting here is that the impact isn’t necessarily direct. Real estate assets are generally priced based on cap rates, but a cap rate (i.e. let’s loosely define them as the going in return an investor is willing to accept to buy a building) builds in many assumptions .. one of which is debt!

So you can now see a clearer relationship here: rate cut → incoming investor can borrow cheaper (debt service is lower) → valuations (all else equal) rise which would help improve the equity positions that are currently in distress.

While it’s possible that sentiment changes would help spur additional transaction volume at higher valuations thereby helping existing distressed positions, there are a few important caveats:

These are “paper” gains.. and the only way to realize some of these increased valuations would be to sell… in the event of equity being wiped out, this likely means that you can’t (or it doesn’t make sense to) sell today and are still dependent on the GP to carry out the mission to (hopefully) get you out at a decent price

See here on misalignment between GP and LP… there are many circumstances where it makes sense to sell an asset, for example, but the counterparty’s incentives point in the other direction

Always keep transaction costs in mind - even if your equity is worth something now, it might not be worth anything once you account for closing costs, the broker fee, and the disposition fee

Since a buyer model that arrives at such an increased valuation has many variables, the sentiment around those variables are critical.

For instance, many rents are flat to down year of year and some investor wonder whether that will continue… this would mean that rent growth assumptions are much more conservative, leading to lower valuations than what would’ve been otherwise possible.

There are similar concerns around rising expenses. If an incoming buyer is assuming higher expenses in the future, there’s less cash flow over the investment period ultimately leading to a lower valuation.

So, in summary, I do not think that a rate cut will materially help LPs that have wiped out equity positions today. I think the same is true about a 50 bps cut. Once you get into 100 bps+ range, I think the impacts will be more meaningful.

There’s no question that rate cuts are net positive news for LPs, but I hope this reminds you to heave a healthy dose of skepticism (see #1 here) if your GP is overplaying/selling the benefits of these cuts for your investment, particularly if it’s in connection to a capital call request (see here for 6 steps to a successful capital call decision).

I hope this was helpful! As always, would love to hear any questions or comments and wishing you a wonderful day.

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos in 4 weeks together with me and other LPs to learn how to find good LP investments.

LP Topics Seminar** - **an ongoing biweekly 1 hour meeting with other LPs where we'll go over investment decks, capital calls, distressed situations, and modeling. This is meant to provide a deeper look into existing LP investments. Please reply to this email if you’re interested.

***LP Community - ***free 2,200+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can reach me at aleksey@hey.com.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.