Aleksey Chernobelskiy

•December 3, 2024

Does the pref even matter?

A deep dive on preferred returns in syndicated LP investments

Welcome back and I hope you all enjoyed the long weekend.

Today I’d like to deep dive on the topic of preferred returns (also referred to as pref), something I find to be often deeply misunderstood among LP investors.

We’ll cover three topics:

What is a pref (and more importantly what it’s not!)

Why you can’t look at a pref in a vacuum

Isn’t a 90/10 split with no pref better for the LP than 80/20 with 8% pref?

AKA “to pref or not to pref” 😊

We’ll run through these in detail and I’ll also provide a graphical example to illustrate a point on the third topic.

Announcements (article continued below):

**Last premium post: **The Dark Side of Masterminds - a peek inside mastermind communities and how to avoid the bad ones

LP Topics: an advanced ongoing biweekly 1 hour meeting with other LPs where we'll go over investment decks, capital call / distressed situations, and modeling. Please reply to this email if you’re interested.

What is a pref (and more importantly what it’s not!)

Simply said, a pref is a preference in payments to the LP before a split (promote) kicks in

Very importantly, notice that a pref is not guaranteed - more on “guaranteed” red flags here

Furthermore, the pref is often not paid in cash in a given year but rather accrued until there’s enough cash to pay it. Of course if the investment generates to pay enough cash then paying the pref will take first priority beyond any operational / capital planning needs

As a retail LP investing in real estate, your mind should “default” to an 80/20 split with an 8% pref as the expectation

If one of these variables is worse to the LP, you should immediately look for the other variable to see if that one got better than the standard

Note that, all else equal, as the risk of a deal increases terms to LP should also improve

You’ll notice that in Top 15 Syndication Mistakes I gave a buffer on these numbers, but that’s because these weren’t reasons to pass on a deal by itself - in other words the pref and split are just one aspect of what you need to realize and I specifically didn’t mention it in the list of 6 reasons to put down a deck

Why you can’t look at a pref in a vacuum

A pref is just one component of the the alignment of interest pillar in LP investments - it’s simply one piece of a single pillar in a three pillar system:

The other two pillars are Execution and the Property itself, and I would suggest thinking of them independently of whatever you arrive within the Alignment of Interest pillar

Comparison across deals within the Alignment of Interests pillar is important and encouraged as I wrote in the introduction here, but you must do so while keeping all of the alignment of interests variables in mind:

Coinvest

Waterfall (which would include both Pref and the Split)

Fees

Therefore, you shouldn’t pick one deal over another because one of them has a higher pref … at **minimum **you should look at the split because the two are very related and cannot be analyzed separately

For example… you might get excited about a 10% pref, only to realize that the split is 30/70 - 30% to the LP! Vice versa, you could pass on a deal that doesn’t have a pref whatsoever, not realizing that the split is 90/10 (more below on this) or better

Isn’t a 90/10 split with no pref better for the LP than 80/20 with 8% pref? AKA “to pref or not to pref”

The short answer is that they’re actually fairly close in terms of performance, as we’ll see below

If you feel very strongly about the downside risk of the investment, the 90/10 will actually benefit you as an LP above a certain multiple. However, downside risk is hard to predict.. and therefore I would usually guide LPs to invest with a pref for that reason - real estate investments aren’t here to make you 10x returns, so you should be that more careful about protecting your downside (see more on this risk/reward discussion here).

Let’s run through an example now to illustrate the above:

An LP invests $500k

They have an option to invest using a (1) 90/10 with no pref and (2) 80/20 with 8% pref structure

Let’s assume a 5 year hold with no pref payments during the investment horizon

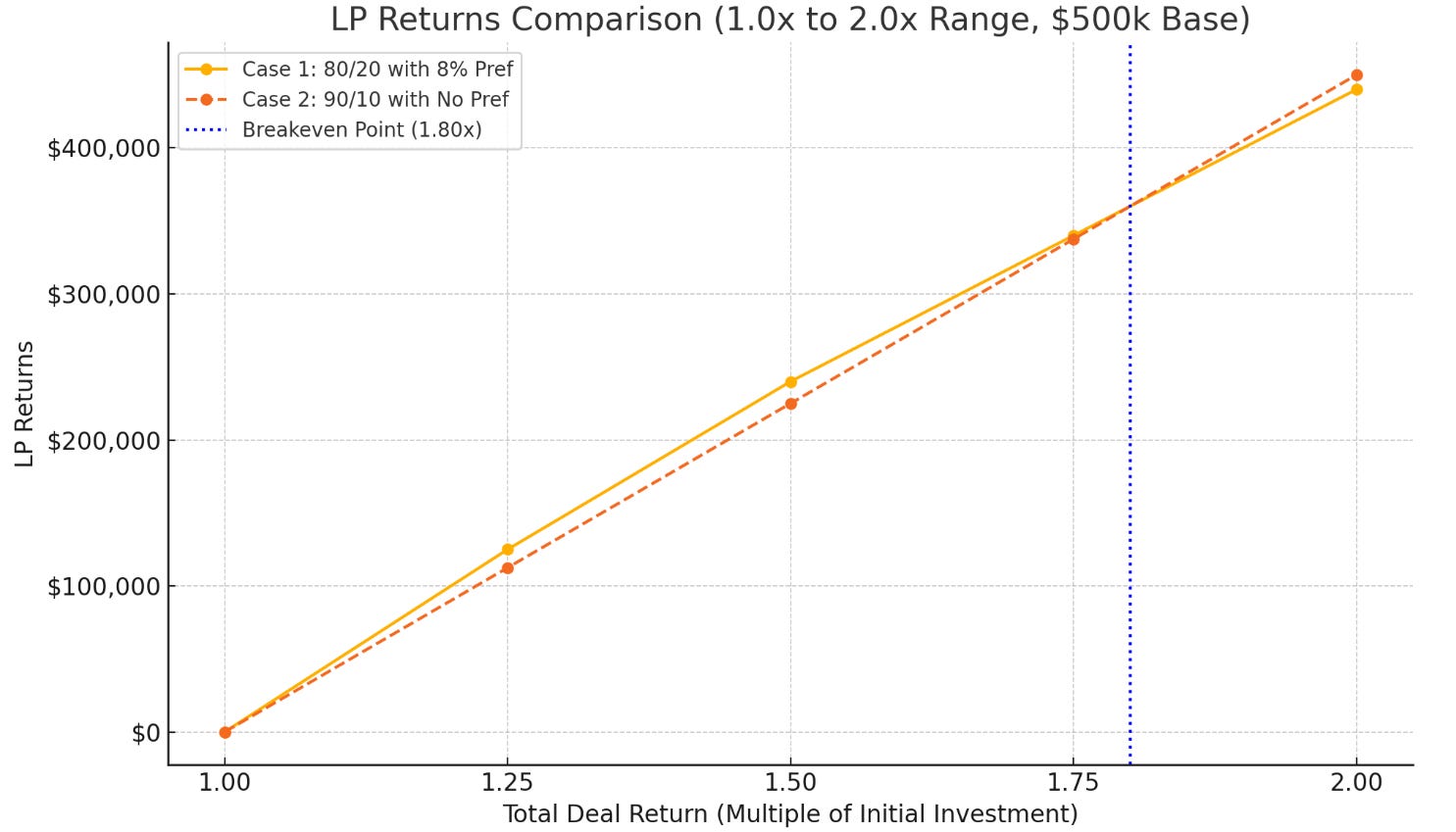

How will the returns to the LP vary depending on performance? 🤓

Below you’ll see two plotted lines - here’s a quick analysis and conclusion:

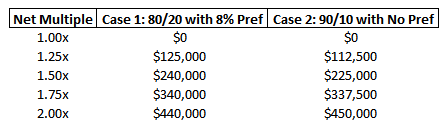

To get grounded, if you just get 500k back that’s return of capital or a 1x return and the GP gets nothing … and there’s no return to you as an LP either (i.e. $0 on Y axis).

If you got a 1.5x return, that would mean that there’s 250k that has to go through the waterfall:

90/10 with no pref: there’s no pref.. so you simply get 90% of 250k which is $225k - you’ll see that plotted below at 1.5x in the orange dotted line

80/20 with 8% pref structure:

There’s 8%5$500k = $200k in accrued pref to date (remember - 5 year hold period with no cash payments in the interim) .. which means before the split kicks in the first $200k of the $250k would go to you as the LP and only the remaining $50k gets split 80/20 (i.e. you’d get another $40k)

Total proceeds of $200k+$40k = $240k, which is why the yellow line (Case 1) is higher than the orange one below

You can follow this logic to see that the breakeven point occurs at 1.8x multiple… beyond which (this is a pretty serious upside) it’s better to be an LP with the no pref structure

Try to calculate this 1.8x breakeven point yourself, it’ a good quick exercise - the proceeds should be exactly $360k in either scenario.

Note that this exercise ignores all entry and exit fees, which can be very material and erode equity … further highlighting that a pref is an important tool to protect your downside as an LP

Final note is that notice that I used splits that were fairly close to one another (80%→90%) .. the further the distance between these, the more these outcomes will get extreme and so you have to remember to pay close attention to the details

I advise LPs on existing and potential positions and write articles here weekly on what I see in the marketplace that could help you invest better. You can find me on LinkedIn or Twitter.

Whether you’re an LP, want to learn to become one, or affiliated with LPs (GPs, Attorneys, CPAs, Financial Advisors) I hope you’ll consider subscribing and sharing this post to help others make more informed investment decisions.

When you’re ready, I could help you in 3 ways - simply reply to this email if one is of interest:

Limited Partners:

Potential positions - you’re considering investing and need an independent opinion

Existing positions - there’s a lack of communication, you’re concerned about fraud, or perhaps you got a capital call request and you’re not sure how to proceed. I have also helped LPs with a “post-mortem” analysis on deals that didn’t work out - it’s important to learn these lessons as opposed to just blaming the GP.

LP Course - review 4 separate memos in 4 weeks together with me and other LPs to learn how to find good LP investments.

LP Topics Seminar** - **an ongoing biweekly 1 hour meeting with other LPs where we'll go over investment decks, capital calls, distressed situations, and modeling. This is meant to provide a deeper look into existing LP investments. Please reply to this email if you’re interested.

***LP Community - ***free 2,500+ member LP Investor community on Twitter

***Find GPs ***in unique asset classes/geographies on my monthly intro post (see LinkedIn’s post as well for more)

General Partners:

Deck review - I’ll look over your marketing materials from the perspective of an LP and provide slide by slide commentary to improve your pitch

Investment review - I’ll provide independent feedback on an opportunity you’re pursuing

Capital call advisory** - **you suspect that you’ll need to make a capital call, but aren’t sure how to proceed or communicate the message.

Other - anything from waterfall/fee advisory to disagreements between co-GPs on the proper path given a set of circumstances

General Consulting: modeling, strategic advisory, underwriting training, etc.

If you’d like to speak on the phone, you can reach me at aleksey@hey.com.

Join GP-LP Match

Connect with GPs and access exclusive investment opportunities on our platform.

100% free. No credit card required.